AT A GLANCE

- PSD3 and the PSR move more scam liability onto PSPs and strengthen fraud-prevention duties.

- Verification of Payee is becoming mandatory on the timelines set by the Instant Payments Regulation, including 9 October 2025 for euro-area Member States.

- Instant payments compress decision windows from hours to seconds, making post-settlement reviews far less effective. This is an inference from the instant-payments rollout and the regulation’s emphasis on real-time controls.

- Credit transfer fraud losses reached €2.2 billion in 2024, up 16% year on year.

- PSPs now need stronger real-time monitoring, faster customer interventions, and tighter refund operations.

- The firms best positioned for 2026 are the ones with unified fraud, AML, and case-management workflows.

New PSD3/PSR Fraud Prevention Obligations

European regulators are overhauling payment rules to clamp down on scams and fraud, introducing sweeping obligations under the proposed Payment Services Directive 3 (PSD3) and an accompanying Payment Services Regulation (PSR). The new framework greatly expands fraud refund liability for Payment Service Providers (PSPs) and mandates proactive anti-fraud measures. For example, PSPs will be liable to cover customers’ losses if they fail to implement appropriate fraud prevention mechanisms. Critically, providers must verify that a payee’s name matches the account identifier (IBAN) before executing a transfer, a Verification of Payee (VoP) requirement. If there’s a mismatch, the PSP is obliged to refuse the payment and alert the payer. This IBAN-name matching (similar to the UK’s Confirmation of Payee) is set to become a standard safeguard across Europe, aiming to thwart Authorized Push Payment (APP) scams where victims are tricked into sending money to fraudsters.

Liability for scams is also shifting squarely onto PSPs. In cases of impersonation or social engineering fraud, for instance, a scammer posing as a bank employee to convince a user to approve a payment, the PSP will generally have to refund the full amount as long as the customer reports the fraud to the police and informs the PSP. PSD3 makes it unequivocal that consumers should not be left out-of-pocket from such scams. This mirrors the approach taken in the UK’s recent APP fraud reimbursement rules, essentially eliminating ambiguity over “who pays” when a customer is duped. Unless there is evidence of gross negligence or collusion by the customer, the default expectation is victim reimbursement, with PSPs and other players in the ecosystem (even online platforms or telecom providers) potentially sharing the burden.

Beyond refunds, preventive measures are now mandatory. The PSR deal confirms that PSPs must implement “appropriate fraud prevention mechanisms” and conduct risk assessments on transactions, or else face liability. Strong Customer Authentication (SCA) remains crucial, but regulators acknowledge that fraudsters are exploiting human factors and SCA exemptions. Thus, PSD3/PSR explicitly empower PSPs to act on fraud signals: providers will have the right (and obligation) to block or delay a payment if their systems detect strong evidence of fraud in progress. This is a significant shift from the previous regime where banks often felt obliged to execute even suspicious authorized payments. In short, under PSD3/PSR, “faster payments” must be matched by faster fraud defenses. PSPs are expected to utilize advanced, real-time monitoring and intervene when needed, rather than simply processing transactions and investigating after the fact.

Another notable requirement is for PSPs to offer customers tools to control fraud risk, such as setting spending limits and enabling transaction blocks. These customer-facing features (already used by some digital banks) will now be standard, allowing users to cap their transfer amounts or freeze certain payment types to mitigate fraud exposure. PSPs also must ensure accessible human support for fraud issues (not just chatbots) and contribute to fraud awareness education. Taken together, the PSD3/PSR reforms represent a comprehensive push for the industry to prevent scams upfront and swiftly remediate those that occur. The question is: are PSPs operationally ready to meet these real-time fraud and liability challenges?

Instant Payments Heighten the Fraud Challenge

The urgency of these obligations is magnified by the rapid adoption of SEPA Instant Credit Transfers and other real-time payment rails. Under the EU’s Instant Payments Regulation adopted in March 2024, any PSP that offers standard euro credit transfers must also be able to send and receive instant transfers. By October 2025, virtually all euro-area banks and payment institutions will be live on SEPA Instant for outgoing payments. This infrastructure moves money in seconds, 24/7, drastically shrinking the window in which fraudulent transactions can be intercepted or reversed.

Real-time payments compress every decision window: liquidity moves out immediately, and fraud risks evolve in real time. The traditional approach of reviewing transactions in batch cycles or flagging suspicious activity after settlement is no longer viable when a thief can receive and withdraw funds before a victim even realizes what happened. Instant payments demand instant fraud detection and response. PSPs must scrutinize each transaction on the fly, leveraging live data and advanced analytics to catch red flags within milliseconds, not hours.

The high speed of SEPA Instant also elevates PSPs’ liability exposure under the new rules. If a scam payment is executed instantly and the customer is defrauded, the PSP now faces the prospect of reimbursing that loss rapidly. However, recovering funds from the receiving end is extremely difficult once they’ve moved in real time. This puts pressure on the sending PSP to stop fraudulent payments before they leave the account. Regulators have effectively acknowledged this by allowing sending institutions to pause suspicious transfers despite the “instant” promise. Likewise, receiving institutions are expected to freeze incoming funds that trigger fraud alarms, a critical measure to prevent money mules from quickly dissipating stolen money across other accounts.

The stakes are illustrated by recent fraud data. According to a joint EBA/ECB report, fraud involving credit transfers jumped to €2.2 billion in 2024 (up 16% year-on-year), and the vast majority of those losses (around 85%) were borne by customers themselves, largely due to scams that tricked them into initiating the payment. These figures highlight why regulators are intervening: instant payments have become a fraud vector of choice, where criminals exploit the speed to outrun traditional safeguards. Going forward, the expectation is that PSPs will drastically reduce customer losses in such scenarios, both by preventing scams and by swiftly reimbursing victims. But doing so will require PSPs to operate at a whole new level of agility and coordination.

Operational Gaps: From Real-Time Detection to Refunds

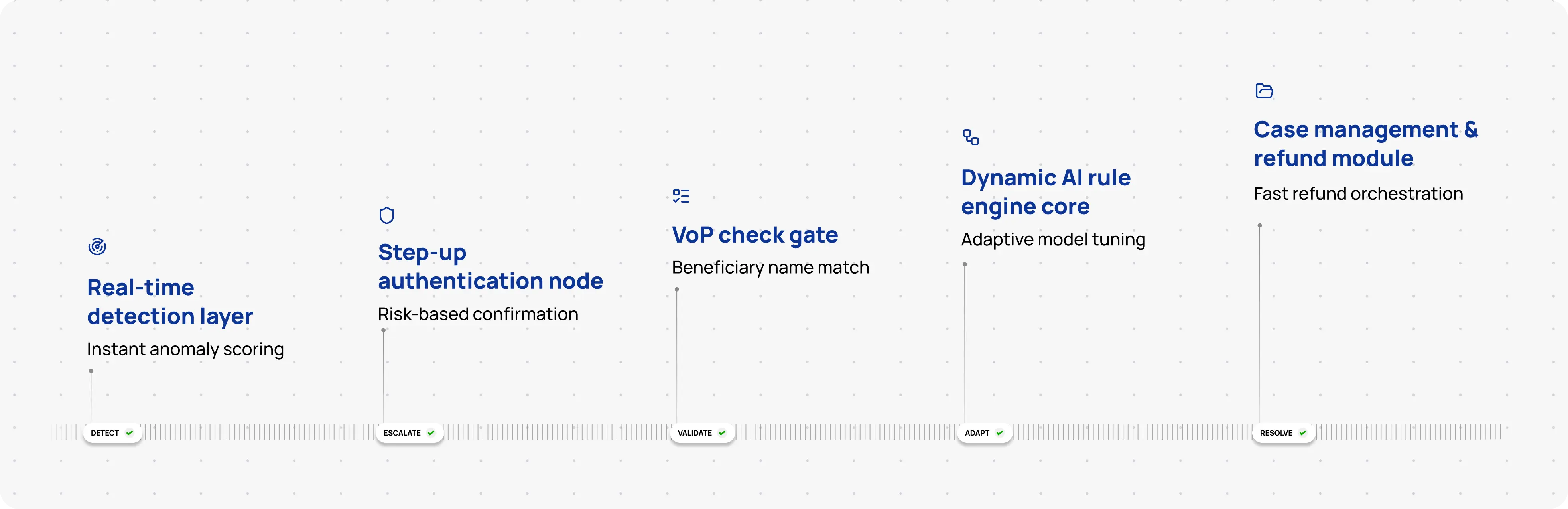

Complying with real-time fraud obligations under PSD3/PSR is not just a policy tweak, but an operational transformation for many PSPs. Key capabilities that firms now need include:

- Real-Time Transaction Monitoring: PSPs must deploy sophisticated systems (often AI-powered) that continuously analyze transactions and customer behavior patterns as they happen. Rules and models should instantly flag anomalies or known fraud markers (e.g. mule account indicators, unusual payment requests) so that intervention can occur before the payment is completed. This is a step up from legacy fraud systems that might only generate alerts after the fact. Leading providers are moving toward multi-layered, real-time risk scoring, evaluating device, behavior, and contextual data in milliseconds to assign a fraud risk score to each transaction. Such dynamic scoring is necessary to catch fast-evolving scams without flooding operations teams with false positives.

- Stepped-Up Customer Confirmation: In cases where fraud indicators are moderate (not certain), PSPs may consider “stepping up” the verification before executing a risky payment. This could mean an extra prompt to the customer (e.g. confirming a suspicious payee via a second channel, or a phone call from the bank’s fraud team). PSD3’s allowance for transaction blocking/delay gives PSPs latitude to build in these friction steps when merited. However, implementing this effectively requires finely tuned risk models, you don’t want to introduce too much friction and inconvenience legitimate customers. Many firms are now exploring risk-based authentication triggers, where only truly high-risk instant transfers get slowed down for additional checks.

- VoP Integration (Verification of Payee): By October 2025, PSPs must integrate an interbank name-check service into their payment flows. Operationally, this means whenever a customer enters a new payee’s account number, the PSP’s system should automatically query the beneficiary bank to compare the payee’s name with the account holder name. The customer should be alerted in real time to any mismatch (“no match” or significant discrepancy) before the payment is executed. Many banks in the EU are now connecting to shared VoP utilities (some provided by central banks or vendors) to fulfill this requirement. The challenge is ensuring this process is fast and seamless within the instant payment UX. PSPs will need to handle cases where the name partially matches (e.g. minor spelling differences) by giving clear warnings or guidance to users. Importantly, under PSR the onus is on the PSP to refuse the payment if there’s a clear mismatch that signals fraud. Integrating this check and business logic into core banking systems and online banking apps is a non-trivial project that many institutions are racing to complete.

- Dynamic Rule Tuning and AI Analytics: Fraud patterns mutate rapidly (social engineering schemes, mule account networks, etc.), so PSPs must move away from static rules that are hard-coded or rarely updated. Regulators and industry experts now stress adaptive fraud prevention that can learn and adjust in real time. This could involve machine learning models that identify anomalous behavior that doesn’t match a customer’s normal profile, or AI tools that suggest new rule thresholds to minimize false positives. An important operational practice is to continuously tune detection rules based on feedback: for example, if certain alerts are consistently false alarms, refine or replace that rule. Conversely, if a fraud incident slipped through, back-test and create a rule to catch similar cases going forward. Firms should invest in analytics platforms where fraud analysts can simulate rule changes on historical data and deploy updates swiftly (with proper governance). The goal is a “living” fraud defense that evolves as fast as the fraudsters do. As one expert noted, many banks historically only updated fraud rules after major incidents or audits, a reactive posture that won’t suffice now. Going forward, PSPs need agile processes to update risk models perhaps daily or weekly, not yearly.

- Fast Refund and Case Management Workflows: Meeting the refund obligations (e.g. refunding an APP scam victim once they report) demands an efficient internal workflow. PSPs should establish a unified case management system for fraud claims, where alerts, investigation notes, and reimbursement decisions are all tracked. When a customer reports an unauthorized transaction or scam, the clock starts ticking. Under PSD3, unauthorized payment claims must be investigated and refunded within 14 business days in many cases. For authorized scam cases, the expectation is also for prompt provisional refunds once basic checks (like confirming the customer filed a police report) are satisfied. This requires operations teams (fraud, compliance, customer support) to work in concert. A best practice is to have a dedicated fraud incident response team that can rapidly gather the facts (Was SCA bypassed? Did the PSP’s controls flag anything? Is the beneficiary account identifiable for recovery?) and make a reimbursement decision. Automating parts of this workflow can help; for instance, an alert triggered by the customer’s fraud report could automatically pull relevant transaction details and risk scores into a case file. Some PSPs are also implementing metrics to track their fraud response times and refund rates, as seen in the UK after mandatory APP reimbursements. Regulators will likely scrutinize how quickly and fairly PSPs handle victim compensation, so having a well-oiled case management process is essential.

Unfortunately, many PSPs still have gaps in these capabilities. Legacy banks might rely on siloed fraud systems that flag basic rule breaches (e.g. transfers over a certain amount) but miss clever social engineering scams. Fintech startups may have tech-savvy platforms yet lack mature fraud operations or data-sharing arrangements with other institutions. Across the board, a common challenge is breaking down data silos, fraud signals might reside in one system (transaction monitoring), customer due diligence info in another, and case tracking in yet another. To respond in real time, PSPs need integrated views of customer risk and the ability to orchestrate data from multiple sources instantly. This is pushing many firms to reevaluate their technology stack and consider more unified solutions, as discussed later.

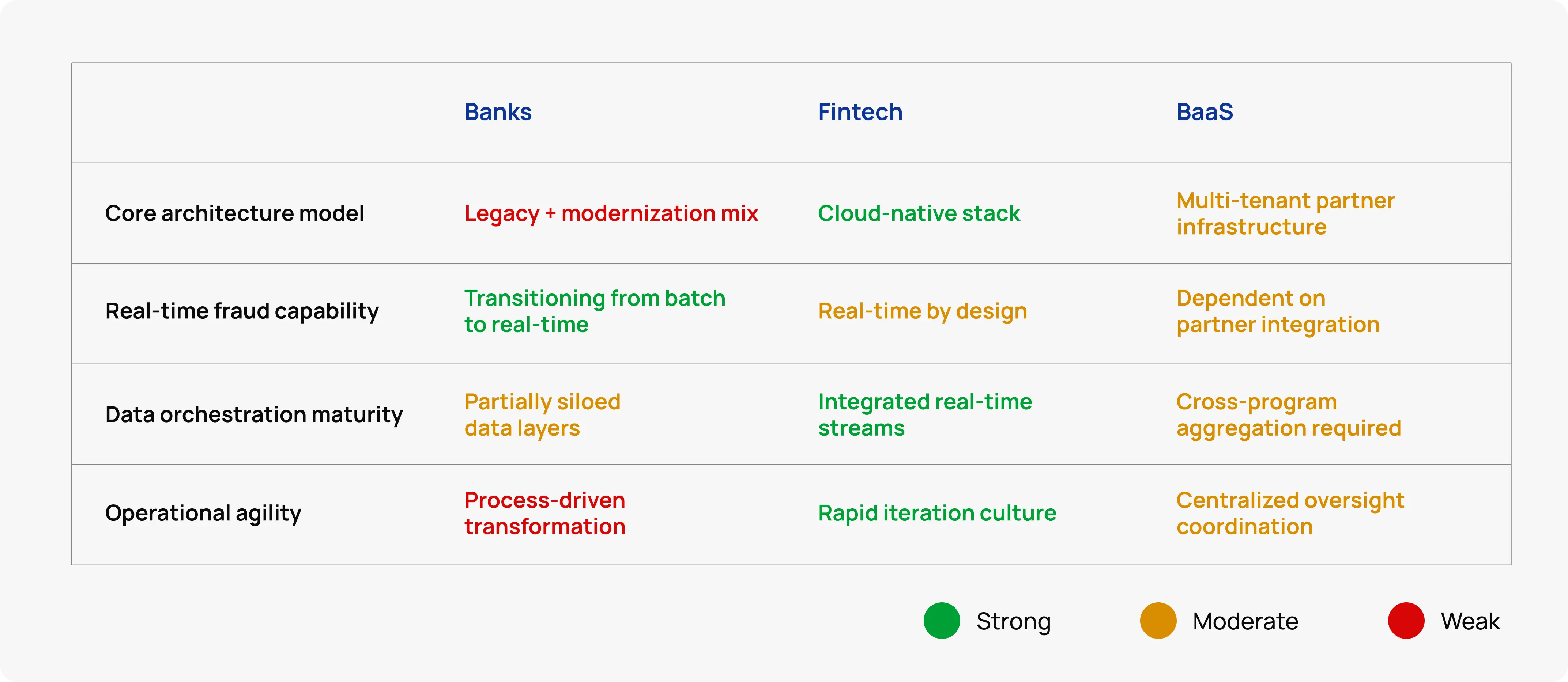

Banks vs. Fintech vs. BaaS: Who Is Ready?

Operational readiness for these new fraud rules varies widely across different types of PSPs:

- Traditional Banks: Many incumbent banks are in the midst of digital transformation, but they still contend with legacy core systems not designed for 24/7 real-time processing. These older systems often rely on end-of-day batch reconciliations and have limited real-time analytics, creating a “real-time bottleneck” in fraud detection. For instance, a bank’s mobile app might allow instant payments front-end, but the back-end fraud review might be batch-based, causing latency in catching issues. On the upside, large banks have established fraud units and sizeable budgets. Many are now investing in modernizing their payment hubs and fraud tech. Leading banks are consolidating payment processing into unified, API-driven platforms and embedding AI into payment flows for smarter fraud detection and dynamic risk scoring. However, organizational inertia can be a hurdle; changing internal processes (like empowering front-line staff to block suspicious payments immediately) may require significant cultural shifts and training. Legacy banks also tend to have stricter compliance checks which, if not tuned, could introduce friction or slow responses. In summary, while big banks have the resources and have begun upgrades, some are playing catch-up to match the agility that instant fraud prevention demands.

- Fintech and Neobanks: Digital-native fintech companies and challenger banks generally have more modern infrastructure and a culture of rapid iteration. Many fintechs built their stack using cloud-native services and real-time data streaming, which can make it easier to plug in advanced fraud detection tools. They often excel at customer experience, which includes things like instant notifications and in-app controls (features that align well with PSD3’s fraud tools mandate). Some fintechs already provide features like freeze your account with a tap, or automated warnings if a transfer looks fishy. That said, fintechs vary widely in their fraud management maturity. A smaller fintech might lack a dedicated fraud team or sophisticated models, initially relying on basic rule engines. As they scale, they face the same challenges as banks in detecting complex scams. Another consideration is that fintechs often partner with sponsor banks or BaaS providers for licenses; they need to ensure fraud data flows between the fintech and its bank partner in real time. Fintechs tend to be more nimble in deploying new technology (e.g. adopting machine learning solutions quickly), but they must ensure they meet the rigorous compliance standards that regulators will enforce. In the best cases, fintechs are turning fraud prevention into a competitive advantage (advertising how safe and quick to respond they are), which could put pressure on slower-moving incumbents.

- BaaS Platforms and Sponsor Banks: Banking-as-a-Service providers (and the sponsor banks behind many fintech programs) face a unique set of challenges. They operate multi-tenant platforms serving many fintech or corporate partners, which means fragmented data sources and tools if not managed carefully. In fact, a common issue in BaaS models is the use of multiple disconnected compliance and fraud systems across different programs. One fintech partner might use a third-party fraud tool and report alerts to the sponsor bank in a spreadsheet, while another fintech uses a different approach; the sponsor bank then has to aggregate these inputs to have an enterprise view. Such silos make it hard to detect cross-platform patterns (e.g. the same mule account receiving payments from multiple fintechs) and can slow down response since data isn’t unified in real time. With regulators now scrutinizing bank-fintech partnerships more closely, sponsor banks are expected to have full oversight of their fintech partners’ fraud controls. The best prepared BaaS players are investing in centralized fraud dashboards that ingest data from all partners and apply real-time analytics across the board. They aim for “single pane of glass” monitoring where a risk officer can see alerts and fraud trends for each fintech program and for the portfolio as a whole, updated continuously. BaaS providers also need scalable case management, because a surge of fraud across multiple fintech clients could otherwise overwhelm them. Some innovative BaaS platforms tout their fraud and compliance capabilities as a selling point, offering fintech clients built-in AI-driven fraud detection and unified customer risk profiles. In summary, readiness in the BaaS sector hinges on data orchestration, those who have modern, unified systems will cope far better with real-time obligations than those relying on patchwork reporting from fintech partners.

In practice, no segment is completely ahead or behind, pockets of innovation and laggards exist in each. We see incumbent banks partnering with regtech startups to modernize, fintechs hiring seasoned fraud experts to bolster their defenses, and consortiums forming to share fraud intelligence across institutions. However, as of 2025, it’s fair to say that many PSPs are not yet fully prepared for the speed and coordination that PSD3’s fraud rules demand. The next section looks at how regulators are likely to judge PSPs’ performance and where firms should focus their improvements.

Rising Supervisory Expectations and Data Oversight

European supervisory bodies have signaled that they will be closely watching how PSPs implement these fraud measures, and not just on paper, but in tangible outcomes like reduced fraud losses and faster response times. The European Banking Authority (EBA) already collects detailed payment fraud statistics from PSPs under PSD2, and this will continue under PSD3/PSR with even more focus. The latest EBA-ECB joint report on payment fraud highlighted stable overall fraud rates but rising losses, especially from scams. Regulators noted that strong customer authentication cut card fraud dramatically, but criminals shifted to tricking customers into authorizing payments and exploiting gaps in credit transfers. Notably, in 2024 credit transfer fraud losses hit €2.2B and most of that was due to scams where victims were left holding the loss. This kind of data is a baseline that regulators will expect to improve. Supervisors will want to see the share of fraud losses absorbed by customers come down significantly in the coming years, as PSD3’s liability rules kick in and PSPs enhance their fraud controls.

We can anticipate more rigorous reporting and audit of fraud response metrics. PSPs may be required to report how many APP scam claims they received and how quickly customers were reimbursed, similar to the transparency demanded in the UK. The EBA will also likely update its guidelines on fraud reporting and incident notification to align with PSD3. Real-time payments also bring attention from central banks (for system integrity) and the ECB/Eurosystem, which operates the TIPS instant settlement system. Delays or issues in fraud-blocking could become a systemic concern if not handled well, so supervisory pressure will be high.

Another development is the creation of the EU Anti-Money Laundering Authority (AMLA), expected to become operational in 2026. While AMLA’s primary focus is anti-money laundering supervision, its remit overlaps with fraud in areas like monitoring suspicious transactions and money mule networks (which often facilitate fraud). AMLA may take a holistic view of financial crime controls, assessing how major cross-border PSPs handle scam prevention as part of their overall risk management. We already see convergence in regulatory expectations: for example, authorities emphasize that institutions should break down silos between fraud and AML functions, sharing information to combat both predicate fraud and the laundering of its proceeds. A PSP that is slow to freeze a fraudulent transfer not only fails on fraud prevention but potentially on AML obligations to report and stop suspicious flows. Thus, AMLA and national regulators will judge firms on speed and effectiveness, a PSP that consistently lags in reacting to scams could face not just reimbursement costs but also prudential or enforcement consequences for weak controls.

Moreover, supervisory scrutiny will extend to collaboration and data-sharing. PSD3 explicitly facilitates fraud data sharing between PSPs, and regulators will expect firms to use that provision to their advantage. If a mule account or scam beneficiary is identified at one bank, others should ideally learn of it quickly and block payments to it. Industry utilities or shared blacklists may emerge (in line with GDPR constraints) and supervisors will monitor participation. Regulators like the EBA and ECB may also set up platforms to exchange fraud intelligence in real time. A PSP that is a weak link (e.g. slow to report fraudulent accounts on its books or slow to act on alerts from others) will stand out negatively. In essence, regulators are raising the bar: It’s not just intentions or policies that matter, but demonstrable results in fraud reduction and customer protection.

To meet these expectations, PSPs should anticipate more frequent regulatory reviews of their fraud frameworks. Key performance indicators might include average fraud incident response time, percentage of scam losses reimbursed to customers, and the latency of fraud alerts in an instant payment context. Regulators will also check that PSPs are properly using their new powers, for example, are they actually invoking payment blocking when fraud is strongly suspected? Are receiving banks actively freezing suspect funds and cooperating in investigations? In the near future, firms that can’t demonstrate a fast and structured fraud response will find themselves exposed to regulatory criticism or action.

Priorities for PSPs in 2026: Speed, Integration, and Customer Trust

Given the landscape above, fraud, compliance, and product leaders at PSPs should make enhancing fraud operations a top strategic priority going into 2026. Here are key areas to focus on:

- Orchestrate Fraud and AML Teams & Data: Internally, tear down the walls between fraud prevention and AML compliance. Scams often involve money laundering (stolen funds moving through mule accounts), so your fraud analysts and AML investigators should be sharing intelligence and working off a unified data platform. Consider establishing a financial crime fusion center or similar cross-functional task force that monitors threats end-to-end. Technologically, invest in data integration so that all relevant signals (fraud alerts, suspicious transaction reports, KYC info, device fingerprinting, etc.) can be correlated. This holistic view allows quicker, more informed decisions. For example, if a customer starts a €5,000 instant transfer and a device anomaly and a sanctions list hit are both flagged in different systems, only by combining those would you see a full risk picture and stop the payment in time. Unified case management (covering fraud and AML cases) will also help meet regulatory expectations and avoid duplication.

- Implement Real-Time, Adaptive Rules: Make your fraud detection rules as real-time and adaptive as the payments themselves. This might mean upgrading to an event-driven rules engine or an AI-based system that evaluates transactions on the fly. Ensure that your solution supports real-time rule updates without lengthy development cycles. As highlighted by industry experts, firms should adopt transparent, audit-ready systems that can adjust detection rules in real time as new patterns emerge. Aim for a balance between automated machine learning models (useful for uncovering subtle patterns) and human-tuned rules (useful for domain knowledge and regulatory transparency). In practice, fraud teams should regularly review rule performance dashboards and have a process for rapid tuning, for instance, using champion/challenger rule testing to safely deploy improvements. The ability to quickly introduce a new rule (say, blocking a particular scam phrase in payment references or flagging a surge of payments to a new payee) can dramatically reduce fraud spread. Regulators have signaled they value agility here; showing that you can react within hours or days to a new scam MO (modus operandi) will inspire confidence.

- Enhance Customer Interaction and Education: Every PSP should strengthen the customer-facing side of fraud prevention. This means providing easy-to-use controls like the ability to set transaction limits, disable certain transaction types (e.g. international transfers) via self-service, and instant notifications of payments. Many newer banks already let customers toggle settings (like “block all new direct debits” or “allow transfers only to known payees”); these features can prevent fraud or at least limit losses. Additionally, streamline the process for customers to report fraud or scams, a clear “Report Fraud” button in the app, dedicated phone hotlines, etc. When a customer does report an APP scam, have a compassionate and swift response protocol. This not only meets regulatory requirements but also helps maintain trust (vital in a scam scenario). On the education front, PSD3 mandates more public awareness efforts, so PSPs should proactively send out fraud warning tips, run in-app educational snippets, and train customer service to advise users on fraud avoidance. An informed customer is the first line of defense against social engineering. Ultimately, a PSP that visibly “has the customer’s back”, by both preventing many scams and promptly refunding the occasional victim, will earn loyalty in a market where trust is paramount.

- Prepare for Reporting and Audits: Firms should be ready to demonstrate their fraud prevention efficacy with data. Put in place robust fraud incident tracking and analytics. For example, track the timeline of a fraud case: when was it first flagged by the system, when was action taken, how long did reimbursement take, etc. Measure key stats like fraud losses as a percentage of transaction value (and try to keep it decreasing), average time to block a suspicious transaction, and percentage of scam victims made whole. These metrics will likely be requested by regulators (or at least in supervisory questionnaires). Also, ensure that mandatory reports, such as the PSD2/PSD3 fraud report to regulators, are accurate and complete. Any under-reporting or inconsistencies will raise red flags with authorities who now compare industry data. Internally, use these metrics to drive accountability: perhaps set targets (e.g. respond to 95% of fraud alerts within an hour, reimburse scam claims within 5 days on average) and monitor progress. What gets measured gets managed, and showing improvement over time will be important to both regulators and your own board/executives.

- Collaborate and Share Intelligence: Take advantage of the new legal ability to share fraud information with other institutions. Join or form networks (via industry associations or technology platforms) to exchange data on confirmed fraud cases. For instance, if you identify a mule account or a scam phone number, consider mechanisms to alert others (through a trusted network or perhaps via the central fraud data collection that might emerge from EBA). Collaboration can also include participating in joint fraud drills or information-sharing forums facilitated by regulators. The payoff is a broader view of the threat landscape; many fraud schemes hit multiple banks in succession, so early warning is gold. In the same vein, partner with tech providers and even telecom firms as needed. PSD3 specifically calls on telecom companies to cooperate (to fight SIM swap and spoofing scams), so PSPs should forge those links (e.g. quick channels to verify if a caller is on the actual telecom network origin). The era of fighting fraud in isolation is ending; the winners will be those who join forces across the ecosystem.

Unified Platforms: Turning Compliance into an Advantage

.webp)

Amid these shifts, one trend gaining momentum is the adoption of unified financial crime platforms, solutions that bring together fraud detection, AML monitoring, case management, and even customer remediation in one place. Instead of juggling separate systems for fraud scoring, AML transaction monitoring, KYC screening, and case tracking, PSPs are looking to converge these capabilities. The benefits are compelling: a unified platform breaks down data silos, enabling richer risk assessments and faster decisions. For example, a modern “FRAML” (Fraud + AML) platform can analyze a customer’s profile and behavior across fraud and AML risk factors simultaneously, improving accuracy and reducing duplicate alerts. According to industry research, over half of mid-sized banks have already started converging their fraud and AML systems, reporting not only cost savings but also better detection accuracy and improved regulatory compliance outcomes.

Critically for PSD3 readiness, unified platforms often come with real-time risk engines and alerting built in. They are designed to handle streaming payment data and apply machine learning models or rules within a few hundred milliseconds. This means a suspicious transaction can be flagged (or even auto-declined) almost instantly as it flows through the system, meeting the need for split-second intervention. Modern platforms also support contextual alerting, for instance, if an alert triggers for a possible scam, the system can automatically cross-reference whether the customer was recently a victim (or if related accounts are involved), giving analysts a head start.

Integration of refund workflows is another advantage. Rather than treating reimbursement decisions as a completely manual back-office process, some advanced solutions embed refund decision logic and tracking. A unified case management module can guide an analyst: “This case is an APP fraud claim, the customer has provided a police report, here are the transaction details and risk scores; click here to approve a refund of €X.” It can then log that outcome for audit and even automate notifying the customer. By streamlining these workflows, PSPs can significantly cut down resolution times, a win for compliance and customer experience alike.

From a strategic perspective, adopting a unified anti-fraud/AML platform is about future-proofing. The regulatory environment is clearly moving toward judging firms on speed and coordination, and a single platform can facilitate both. A unified system makes that feasible by pooling all data and decisions in one brain, so to speak. Additionally, it provides a clear, consolidated audit trail that can be shown to regulators to prove the PSP is in control of its risks.

Flagright, as a leading regtech provider, has been a vocal proponent of this unified approach (often referred to as an “all-in-one” financial crime prevention platform). By bringing together transaction monitoring, watchlist screening, case management and more into a single solution, such platforms allow even smaller or newer PSPs to achieve a high level of fraud and scam defense quickly. They come with pre-built real-time rules, machine learning models, and data integrations that can drastically reduce implementation time. For a legacy bank, migrating to a unified platform might be a larger project, but many are considering phased approaches (for example, layering the new platform on top of existing cores as a real-time risk orchestration layer). Fintechs and BaaS providers, on the other hand, often see unified financial crime platforms as a way to leapfrog traditional banks in compliance maturity, turning what could be a heavy compliance burden into a differentiator. By leveraging a cutting-edge platform, a fintech can say: “We may be new, but we have bank-grade (or better) fraud prevention built-in,” reassuring partners and regulators alike.

Ultimately, technology alone is not a panacea, it must be coupled with skilled teams and strong processes. But choosing the right platform can greatly amplify a PSP’s ability to meet PSD3 obligations. Unified, real-time risk engines with integrated workflows ensure that nothing falls through the cracks and that everyone, fraud analysts, MLROs, customer support, is working off the same playbook in real time. As we head into 2026, investing in such infrastructure could be one of the smartest moves for PSPs striving to be compliant, efficient, and trusted in the eyes of customers and regulators.

Conclusion: Speed and Structure Will Define the Winners

The move to instant payments and the new PSD3/PSR rules are collectively raising the bar: no longer will good intentions and basic compliance tick-boxes protect a payment provider from liability or reputational harm. Regulators and customers alike will judge PSPs by how fast and how well-structured their fraud defenses are. Those firms that can spot and stop fraud in seconds, seamlessly coordinate across teams, and make customers whole swiftly will not only avoid penalties, they will build trust and loyalty in an era of digital finance fraught with risks. Conversely, PSPs that remain slow or disjointed in their response will find themselves increasingly exposed. The cost of complacency is rising: beyond reimbursing fraud losses, laggards could face regulatory fines, damaged brand reputation, and loss of business to nimbler competitors. As one analysis put it, the question isn’t whether you can afford to invest in prevention, it’s whether you can afford the cost of falling behind.

The writing is on the wall. Real-time payments are becoming the norm, and with them comes an expectation of real-time fraud control. PSPs should approach this as an opportunity as much as a compliance chore, a chance to upgrade systems, earn customer trust, and perhaps even gain a market edge by being known as the safest pair of hands. The regulators have set the destination: a world where consumers don’t bear the brunt of fraud and scams. Now it’s up to the industry to execute. In the coming years, we will likely see a divide between those institutions that proactively adapt, investing in speed, intelligence, and structural rigor, and those that struggle to keep up. The former will help set the new standards for fraud prevention (and reap the rewards in customer confidence), while the latter will face mounting consequences. In the end, compliance with PSD3/PSR is not just a legal duty but a litmus test of a PSP’s agility and resilience. The message is clear: as instant payments scale, only the truly instant and well-orchestrated fraud responses will pass muster. Those prepared to intervene fast and decisively will thrive, and those who cannot will be left increasingly vulnerable in the payments ecosystem of 2026 and beyond.