The United Kingdom is moving to bring cryptocurrency businesses into the fold of mainstream financial regulation. In December 2025, HM Treasury confirmed plans to regulate crypto asset firms under Financial Conduct Authority (FCA) rules, just like other financial institutions. Legislation slated to take effect in October 2027 will mark a major shift: crypto exchanges, stablecoin issuers, wallet providers, and other crypto firms will face the same regulatory regime as banks, brokers, and payment providers. This approach diverges from the EU’s MiCA framework and has significant implications for compliance. Below, we break down the key points; scope, timeline, regulatory themes, and differences from MiCA, and outline how crypto companies can start preparing now. We also highlight how modern RegTech solutions like Flagright can help firms meet these new obligations in stride.

Scope and Timeline of the UK’s New Crypto Regime

Which firms are in scope? The UK’s upcoming rules cast a wide net over the crypto industry. Any business dealing in crypto assets or providing related services in the UK will need FCA authorization, similar to other financial services. This includes:

- Crypto trading platforms (exchanges): Operators of cryptoasset trading platforms will be held to standards for keeping trading fair, safe, and reliable. They’ll need robust market surveillance and controls against manipulation.

- Stablecoin issuers and wallet/custody providers: Firms issuing stablecoins or safeguarding crypto assets will face prudential rules and strict governance (the Bank of England is separately crafting rules for systemic stablecoins). They cannot pass on interest from reserve assets to coin holders under the current proposals. Custodians must ensure assets are protected and segregated, much like client funds in traditional finance.

- Brokers, lenders, and other intermediaries: Crypto brokers and lending/staking platforms will be subject to conduct requirements so they act responsibly with customers’ assets. Notably, the UK plans to regulate crypto lending, borrowing, and staking, areas that go beyond what MiCA covers. Even certain DeFi activities won’t escape oversight, if there’s a discernible entity running a “decentralized” protocol, the FCA may impose equivalent obligations on it.

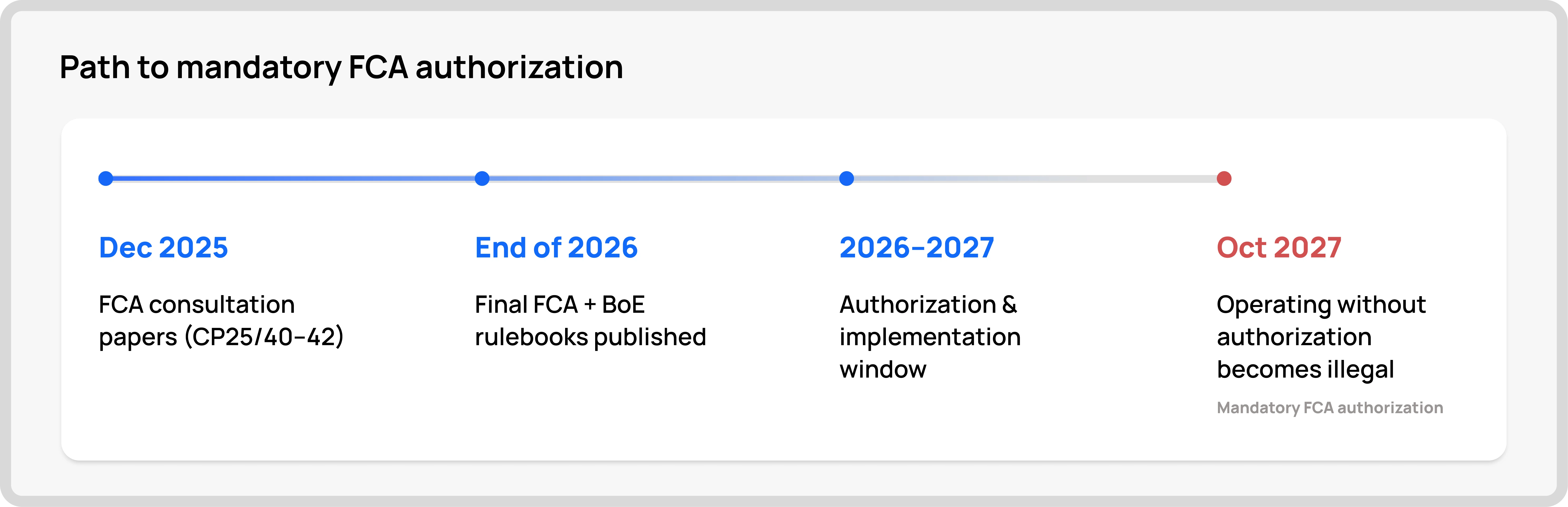

When will this happen? The rulemaking process is already underway. The FCA released a set of consultation papers in December 2025 (CP25/40–42), seeking feedback on detailed rules for trading platforms, disclosures, market abuse, prudential standards, and more. The Bank of England and FCA have committed to finalize their rulebooks by the end of 2026. This gives firms a transition period in 2026-2027 to seek authorization and implement controls. The regime comes fully into force in October 2027, after which operating an in-scope crypto business in the UK without authorization will be illegal. In short, the countdown to compliance has begun, and 2027 is a hard deadline.

Key Regulatory Themes: Consumer Protection, Market Integrity, and AML

The UK authorities have outlined clear objectives for crypto regulation: protect consumers, prevent fraud, maintain orderly markets, and enforce AML laws. These themes echo the principles of traditional financial regulation:

- Strong Consumer Protection: Crypto investors should get the same protections as investors in stocks or other products. The FCA will require clear, factual disclosures when firms list or promote cryptoassets, so people understand the risks before investing. Rules under consideration include applying the Consumer Duty (treating customers fairly) to crypto transactions and possibly giving retail customers access to the Financial Ombudsman for disputes. In practice, expect mandatory risk warnings, transparent terms, and restrictions on misleading ads or overly complex products. As the FCA puts it, regulation should ensure anyone investing in crypto does so “with their eyes open” to the risks.

- Fraud Prevention and Market Integrity: Bringing crypto into the regulatory perimeter is meant to “enhance transparency and oversight,” making it easier to detect suspicious activity and keep out dodgy actors. The new framework will import market abuse controls from traditional markets. Insider trading, pump-and-dump schemes, and manipulation in crypto markets will be explicitly prohibited and punishable, just as they are in stock markets. Trading platforms will need systems to monitor trading patterns and an obligation to report suspicious market behavior. More broadly, firms must bolster their fraud prevention and Anti-Money Laundering (AML) programs, areas that were previously only loosely supervised. The government emphasizes that increased transparency will help “enforce sanctions and hold firms to account where they fall short”, indicating aggressive enforcement against fraud and illicit finance.

- AML and Financial Crime Obligations: The UK has already required crypto exchanges and wallet providers to register for AML supervision in recent years. Under the 2027 regime, crypto firms will be fully subject to the FCA’s AML rules and expectations, just like banks. This means comprehensive know-your-customer (KYC) checks, ongoing transaction monitoring, and prompt suspicious activity reporting to authorities. Firms will also need sanctions screening programs to ensure no dealings with blacklisted individuals or entities. Notably, the Money Laundering Reporting Officer (MLRO) role will be mandatory, the FCA’s proposals designate a Senior Manager for AML (SMF17) at each firm, responsible for compliance. The intent is to close any gaps that criminals or fraudsters could exploit in the crypto sector.

- Prudential Risk Management: To promote orderly markets and firm resilience, crypto companies will face prudential requirements (financial safeguards). Regulators want to ensure that firms have adequate capital or reserve assets, proper risk controls, and plans to wind down in an orderly way if needed. For example, stablecoin issuers might be required to maintain high-quality liquid reserves (potentially even central bank deposits) to avoid collapse. Exchanges and custodians may need insurance or capital buffers to cover operational or cyber risks. By borrowing these prudential tools from traditional finance, the FCA aims to prevent the kind of market chaos seen in past crypto failures and ensure the “orderly wind-down” of troubled firms to protect consumers.

Divergence from MiCA: UK’s Stricter, Centralized Approach

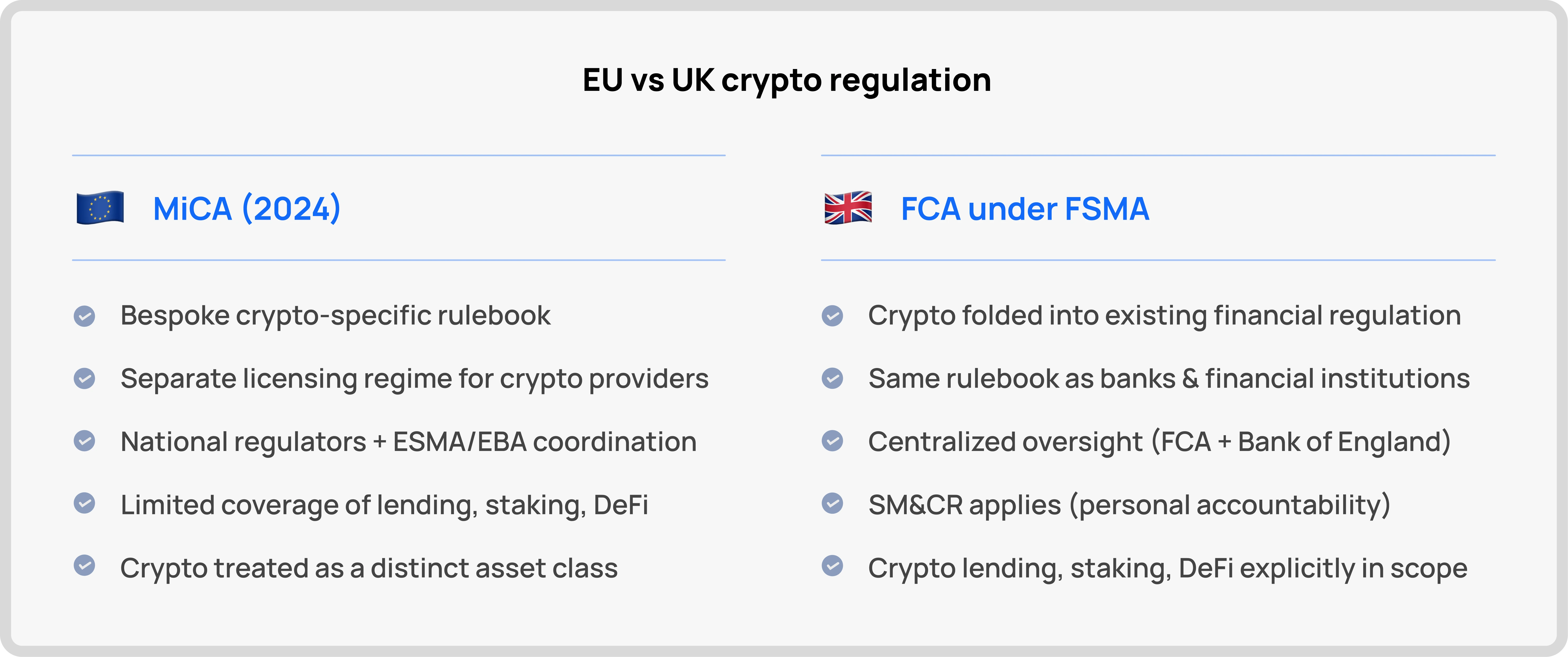

The UK’s strategy is notable for how it differs from the EU’s Markets in Crypto-Assets (MiCA) regulation. MiCA, which took effect in 2024 across the EU, created a bespoke crypto-specific rulebook, essentially a new licensing regime just for crypto service providers. The UK has chosen a different path: rather than a separate crypto framework, it is folding crypto into its existing financial services laws. In practice, this means crypto firms will be regulated as financial institutions under the same FCA rulebook and enforcement structure that applies to banks, securities firms, and payments companies.

“Same risk, same rules”: UK policymakers argue that if crypto activities pose similar risks as traditional finance, they should face similar regulatory outcomes. So crypto exchanges must follow rules akin to securities exchanges; crypto lenders will be treated like other lenders, and so on. The FCA and Bank of England will act as central regulators for the sector, extending their oversight rather than creating a brand-new agency or regime. This aligns Britain’s approach more with the U.S. (which largely regulates crypto through existing securities/commodities laws and banking rules) and less with the EU. In fact, the UK government explicitly framed its law as extending “existing financial regulation” to crypto companies, a pointed contrast to the EU’s purpose-built crypto law.

The result is a more stringent, bank-like regime. By pulling crypto into the Financial Services and Markets Act (FSMA) framework, the UK will subject the industry to the full arsenal of regulatory requirements and powers. For example, firms will have to comply with the FCA’s extensive Handbook rules on systems & controls (SYSC), fit and proper management, and conduct of business. The Senior Managers and Certification Regime (SM&CR) will apply, meaning executives must have clearly defined responsibilities and can be held personally accountable for misconduct. (In practical terms, most crypto companies will need to appoint up to 6 distinct senior manager functions; including a Chief Executive, Chair, Compliance Officer, and MLRO, and ensure they pass FCA vetting.) Such controls mirror those in traditional banking, signaling a major culture shift for crypto startups that once operated in a light-touch environment. As one industry analysis noted, the UK’s move “removes much of the flexibility” that characterized the earlier unregulated phase.

Beyond MiCA in scope: The UK’s proposals don’t just copy-paste the EU rules; in several areas they aim to be tougher or more comprehensive. Notably, by bringing crypto lending, borrowing, and staking into scope, the UK is addressing activities that MiCA left largely unregulated. The FCA is also tackling DeFi with a “substance over form” mindset: if a DeFi platform has identifiable persons exerting control, those persons should bear regulatory responsibility. This hints at a stricter posture on pseudo-decentralized operations, whereas MiCA’s ability to oversee DeFi is more limited for now. Additionally, UK regulators will leverage familiar enforcement tools, from hefty fines and license revocations to potential criminal sanctions for egregious breaches, all of which have precedent in traditional finance enforcement. In short, the UK is creating a centralized, regulator-driven framework that treats crypto much like other regulated sectors, whereas MiCA provides a more self-contained rulebook tailored to crypto specifics. Crypto firms that have dealt with MiCA’s requirements (like obtaining an EU license) will find the UK demands at least as rigorous, if not more so in certain aspects (especially governance and ongoing supervision).

How Crypto Firms Can Prepare Now

With final rules due in 2026, crypto companies have a limited window to ready themselves. Firms that start building compliance infrastructure now will be best positioned to secure UK market access by 2027. Regulators and industry leaders alike are encouraging proactive preparation: as one exchange executive put it, companies have “long awaited regulatory clarity” and can now begin preparing to meet the new requirements. Here are key steps firms should be taking:

Assess and Upgrade Compliance Programs

Perform a gap analysis of your current compliance setup versus a full FCA-regulated firm’s obligations. Many crypto businesses have so far only complied with basic AML registration requirements; this will no longer suffice. Governance structures should be strengthened; e.g., establish a formal board (with independent oversight, if possible), set clear risk appetites, and document compliance policies. Senior management accountability must be formalized (anticipating SM&CR) with designated individuals for compliance, risk, and finance roles. Start inculcating a culture of compliance from the top down, as regulators will expect to see this mindset during authorizations.

Implement Risk-Based Monitoring and Reporting:

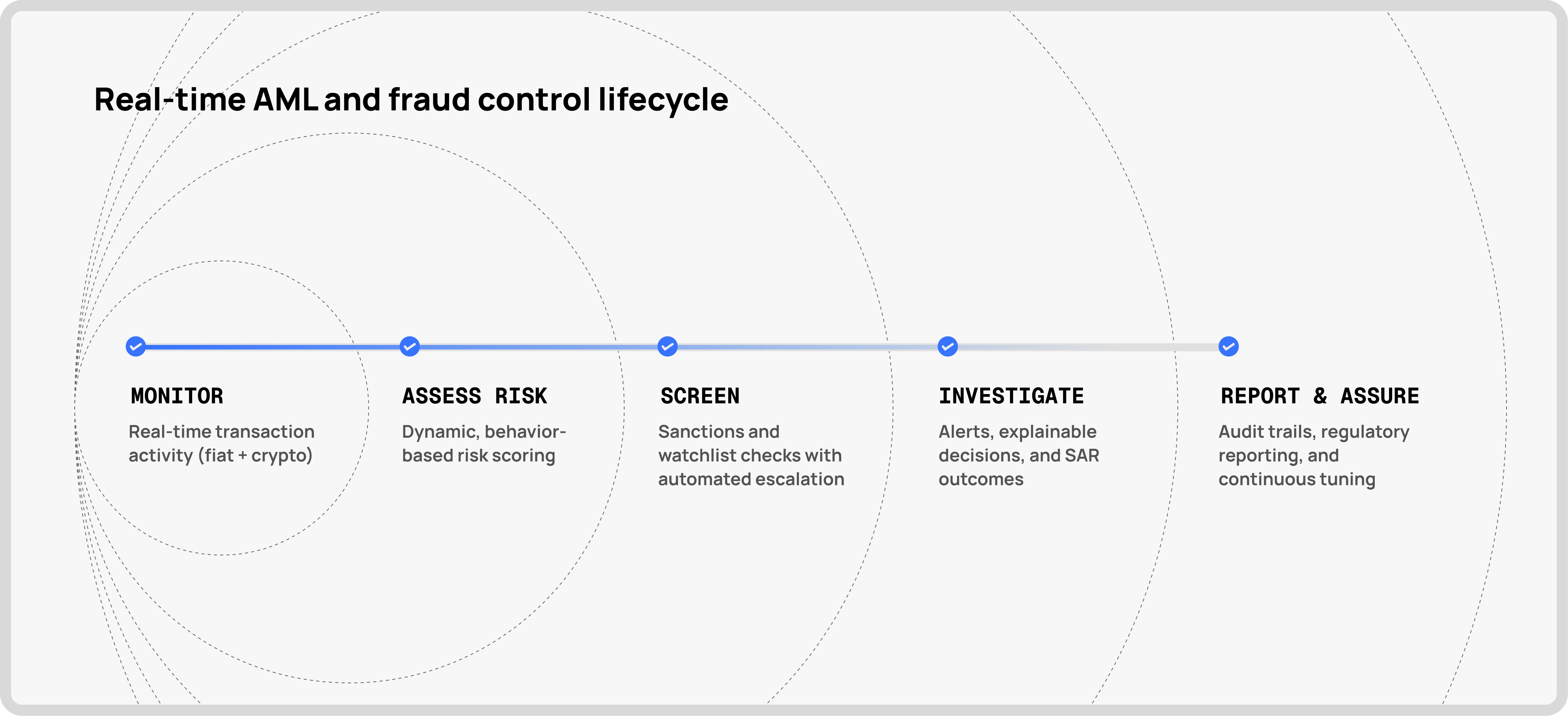

Under FCA supervision, firms must actively monitor transactions and customer activity for signs of money laundering, fraud, and market abuse, and promptly report issues. This requires robust systems to track both fiat and crypto transactions in real time, flag suspicious patterns, and generate alerts for review. Automated transaction monitoring tailored to crypto’s risks (e.g. detecting mixing services or anomalous wallet interactions) should be in place by the time rules hit. Ensure your team can investigate alerts, document their findings, and file Suspicious Activity Reports to the National Crime Agency as needed. In addition, start preparing for regulatory reporting obligations, the FCA may introduce periodic returns for crypto firms (on exposures, reserve assets, client money, etc.), so firms should be ready to compile and submit accurate data.

Enhance Fraud and Financial Crime Defenses

Given the emphasis on consumer protection and fraud prevention, crypto companies should harden their defenses against scams and illicit use. This means strict KYC onboarding (verify customer identities and source of funds), ongoing screening of customers against sanctions and watchlists, and tighter controls on withdrawals or transfers that raise red flags. Consider deploying advanced analytics or blockchain forensic tools to trace crypto flows and identify high-risk transactions. Case management processes are crucial, when an alert or fraud incident occurs, have a clear workflow to escalate it, investigate thoroughly, and take action (like freezing assets or reporting to law enforcement). Firms that can demonstrate a proactive approach to combating fraud and financial crime will not only satisfy regulators but also build trust with customers.

Strengthen Security, Resilience, and Controls

Regulatory scrutiny will extend to operational resilience and IT security, especially for exchanges and custodians that safeguard assets. Start conducting regular penetration tests, security audits, and risk assessments of your technology. Implement rigorous access controls, multi-signature wallets or hardware security modules for custody, and incident response plans for cyberattacks. The FCA will expect firms to be able to “prevent, withstand, and recover” from disruptions or hacks with minimal harm to users. Also, establish business continuity plans and disaster recovery sites, so that even if a system fails, you can continue critical operations. Document all these plans, as you’ll likely need to show them in your license application.

Prepare Clear Disclosures and Customer Communications

In line with consumer protection, review how you communicate risks and product details to customers. Marketing materials and app interfaces should give a fair and balanced view of cryptoasset risks, not just hype. Begin crafting “plain English” risk disclosures for any tokens or services offered, for example, warning that crypto prices are volatile and not covered by deposit insurance, etc. The FCA’s proposed financial promotions regime for crypto (already partly in force) requires risk warnings and prohibits misleading statements. Ensure your compliance team (and legal advisors) vet all public communications. It’s wise to implement a disclosure review checklist now, covering everything from whitepapers to push notifications, to embed fair disclosure practices well before 2027.

Engage with the Regulatory Process

Lastly, don’t stay on the sidelines, engage with regulators and industry groups now. The FCA’s consultations (open until February 2026) are an opportunity to provide feedback or seek clarifications. Participating in industry associations or sandbox programs can help firms stay informed and even influence final rules. The FCA has also been offering pre-application support meetings for crypto firms under the current registration regime; take advantage of these to understand regulatory expectations straight from the source. Early engagement can demonstrate to the FCA that your team is earnest about compliance. It also gives you a head-start in adapting to any nuances in the UK rules (for instance, how exactly DeFi arrangements might be handled, or how the transition for existing registered firms will work). By being proactive, firms signal that they are responsible operators and potentially smooth their path to authorization.

Leveraging Technology for Compliance: Flagright’s Real-Time Solution

Achieving all of the above might sound daunting, especially for crypto startups without large compliance departments. This is where RegTech solutions can play a transformative role. Modern compliance platforms, such as Flagright, are designed to help companies meet regulatory obligations efficiently through automation and AI-driven analytics. In preparation for the UK’s new regime, firms should consider deploying a platform like Flagright to strengthen their compliance infrastructure in the following ways:

- Real-Time, Risk-Based Transaction Monitoring (Fiat + Crypto): Flagright provides an AI-native, real-time transaction monitoring system that covers both traditional fiat payments and on-chain crypto transactions. Firms can configure rules and risk scoring models within minutes (with no coding required) to detect suspicious patterns across their entire transaction flow. Crucially, the system is risk-based, it prioritizes alerts by severity, helping compliance teams focus on the truly high-risk cases (thereby reducing false positives). As UK regulators will expect ongoing monitoring of customer activity, having an automated solution that flags anomalous behavior (e.g. rapid in-and-out transfers, mixing service interactions, abnormal trade sizes) is invaluable. Real-time monitoring means potential issues can be caught and acted upon before they escalate, aligning with the FCA’s goals of prompt risk mitigation.

- Intelligent Alerts with Explainability, Audit Trails, and Approvals: A standout feature of Flagright is its AI Forensics engine that not only generates alerts, but also explains them. Each alert comes with context and rationale; for example, highlighting which rule was triggered or which pattern was detected. This explainability is key for compliance officers (and regulators) to trust and verify the system’s outputs. Flagright also logs a complete audit trail for each alert: when it was generated, who reviewed it, what actions were taken, and the final resolution. Such audit trails will be essential to satisfy FCA examiners that your firm investigates and resolves issues diligently. Moreover, Flagright supports workflow tools for alert handling, including the ability to assign alerts to team members, escalate for senior approval, and track the status through closure. This ensures nothing slips through the cracks and provides documented evidence of your fraud/AML compliance activity; exactly what regulators will look for during inspections or authorization reviews.

- Watchlist Screening and Automated Escalation: Under the new rules, crypto firms must comply with UK sanctions law just like banks do, meaning real-time screening of customers and transactions against sanctions lists (OFSI, UN, etc.) is non-negotiable. Flagright’s platform includes integrated sanctions and watchlist screening, continuously updated, to instantly flag any prohibited parties in your customer base or transaction flow. If a potential match or high-risk entity is found, the system can automatically escalate with a predefined workflow, e.g. pause the transaction, alert the MLRO, and guide the analyst through next steps (like enhanced due diligence or reporting). These escalation workflows can be customized to fit the firm’s policies. Having screening and case handling in one system not only improves efficiency but also provides a clear record that you’ve checked all transactions against sanctions, a point the FCA will likely verify. With the geopolitical climate and focus on cutting off illicit finance, a robust sanctions compliance process (as Flagright enables) is critical to keep “dodgy actors” out of the UK market.

- Unified Case Management and Regulatory Reporting: Compliance isn’t just about finding problems, it’s about documenting and reporting them properly. Flagright offers a unified case management module where all alerts, once investigated, can be compiled into cases. Within a case, analysts can attach their findings, link related alerts or customer profiles, and collaborate on an investigation. This unified view is extremely useful if, say, one customer triggers multiple alerts over time or across different risk areas (fraud, AML, etc.), you can see the full picture in one place. When it comes time to report to regulators (for example, filing a Suspicious Activity Report or an annual compliance return), the relevant information is readily available in the system. Flagright can even assist in generating regulatory reports by aggregating statistics and data from your monitoring program. By centralizing monitoring, investigation, and reporting, a platform like Flagright not only saves time but also ensures consistency and completeness in your compliance output. This kind of well-documented, tech-enabled compliance operation will be a strong asset when seeking FCA authorization, demonstrating that your firm has the tools to meet rigorous supervisory standards.

Product-forward insight: Embracing an AI-driven compliance platform is not just about ticking boxes, it’s about future-proofing your business. The UK regulators favor a “data-driven” and adaptive approach to supervision, and they will expect firms to leverage technology to manage risks in real-time (manual, ad-hoc processes won’t cut it at scale). By integrating Flagright or similar solutions now, crypto companies can streamline their compliance workflows and gain confidence that they’ll detect issues early and accurately. It also frees up your compliance officers to focus on high-level risk management and strategy, rather than being buried in paperwork or reactive firefighting. In summary, smart investment in RegTech today can pay dividends by 2027, as regulators will view tech-enabled firms as more robust and easier to supervise, potentially smoothing the path to approval and ongoing operations in the UK.

Conclusion: Build Compliance Now for 2027 Success

The message from the UK authorities is loud and clear: “Regulation is coming, and we want to get it right.” Crypto firms that aspire to operate in the UK must likewise “get it right” by treating compliance as a first-order priority. The new FCA crypto regime represents a fundamental raising of standards that will reshape the industry’s landscape. Companies that invest in strong compliance programs now, aligning with the themes of consumer protection, market integrity, and financial crime prevention, will reap the benefits when the rules kick in. They’ll earn the trust of regulators sooner, enjoy greater access to banking and partnerships, and be well-positioned to attract customers who feel safer under a regulated umbrella. By contrast, firms that delay changes or hope for looser rules risk scrambling at the last minute or even being shut out of the UK market.

In the bigger picture, bringing crypto under the FCA’s wing is about maturation of the sector. It’s a chance to “boost consumer confidence” and integrate crypto into the mainstream financial system in a sustainable way. For compliance leaders and founders, this is an opportunity to turn robust compliance into a competitive advantage. Those who establish transparent, well-governed operations can differentiate themselves from less prepared rivals and engage with institutional partners who demand high standards. As we’ve discussed, tools like Flagright can catalyze this process, enabling even lean startups to meet big regulatory expectations through smart automation and risk-focused design.

UK crypto regulation may feel complex, but its core premise is simple: same business, same risks, same rules. Firms that internalize this principle and act accordingly will find that 2027 is not a threat, but a milestone that validates their credibility. The road to authorization will involve hard work, bolstering systems, filling compliance gaps, and perhaps redefining business practices, but it will also unlock growth in a market that values trust and compliance. As the UK Chancellor put it, clear rules of the road give firms the certainty to “invest, innovate and create high-skilled jobs,” while safeguarding consumers and keeping bad actors out. By starting the journey today, crypto businesses can ensure they are ready to hit the ground running when the new regime takes effect. In short, build your compliance house now, and you’ll be ready to open your doors to the UK’s regulated crypto future in 2027.