Healthcare payments have become an unexpected front in the fight against money laundering. Long seen primarily as targets for billing fraud or abuse, systems like claims processors, telehealth billing platforms, and pharma payment networks are now being actively exploited to wash illicit funds. In 2025, U.S. authorities sounded the alarm: the Justice Department’s largest-ever health care fraud takedown charged 324 individuals across $14.6 billion in false claims, more than double the prior record via the DOJ’s National Health Care Fraud Takedown announcement. Critically, many of these schemes didn’t just steal from insurers and government programs; they systematically laundered the proceeds through shell companies, crypto assets, and international transfers (DOJ’s National Health Care Fraud Takedown announcement). This marked a shift in enforcement focus, healthcare payment platforms are no longer just a fraud issue, but a growing AML (Anti-Money Laundering) concern. Regulatory bodies like FinCEN and HHS are increasingly urging financial crime scrutiny in health-related flows, recognizing that criminals piggyback on healthcare rails to move dirty money under the guise of legitimate payments, as outlined in Treasury’s FinCEN advisory on fentanyl-related illicit finance. The message is clear: healthtech billing and pharma payment operators must shore up AML controls now, or risk being the weak link that criminals exploit.

Regulators Crack Down: 2025’s AML Wake-Up Call in Healthcare

Several 2025 developments exposed how healthcare financial flows are being misused, and put the industry on notice to strengthen AML measures:

- DOJ Enforcement, “Money Laundering” in Health Fraud Schemes: In June 2025, the DOJ’s National Health Care Fraud Takedown revealed that criminal rings are not only committing massive Medicare fraud, but also integrating money laundering tactics into those schemes. For example, one international network stole patient identities to bill Medicare $10.6 billion for phony medical equipment, then laundered the $900+ million in proceeds via cryptocurrency and offshore shell firms (DOJ’s National Health Care Fraud Takedown announcement). A complicit U.S. banker even facilitated moving the fraud funds abroad while circumventing AML controls (DOJ’s National Health Care Fraud Takedown announcement). In another case, conspirators funneled Medicare payments to their own accounts and then concealed and transferred the money overseas (DOJ’s National Health Care Fraud Takedown announcement), conduct leading to standalone money laundering charges. These takedowns underscore that health payment fraud and money laundering now go hand-in-hand. As DOJ officials noted, this is an “unprecedented” threat exploiting patients and taxpayers (DOJ’s National Health Care Fraud Takedown announcement), demanding a whole-of-government response.

- FinCEN & HHS Red Flags: Financial regulators have amplified the concern. FinCEN reported in August 2025 that over a hundred recent suspicious activity reports (SARs) showed healthcare fraud proceeds intermingling with broader laundering networks, including those tied to foreign money laundering organizations (Treasury’s FinCEN advisory on fentanyl-related illicit finance). This aligns with trends seen in elder fraud and other scams, illicit actors view health related payments as a soft target to hide dirty money flows. HHS agencies, for their part, have ramped up anti-fraud guidance and enforcement of healthcare fraud and abuse laws (like the False Claims Act and Anti-Kickback Statute) which often carry attendant money laundering charges. Notably, HHS’s Office of Inspector General and CMS (Centers for Medicare & Medicaid Services) now emphasize advanced data analytics to proactively flag anomalies in claims and payments (DOJ’s National Health Care Fraud Takedown announcement). Regulators are effectively saying that if you operate in healthcare payments, you must treat AML risks as seriously as fraud risks, the two are increasingly intertwined.

- Trade and Sanctions Concerns in Pharma Payments: Cross-border pharmaceutical transactions have drawn scrutiny from international watchdogs for facilitating money laundering and sanctions evasion. The Financial Action Task Force (FATF) and Egmont Group highlighted trade-based money laundering (TBML) typologies where shell distributors and unusual trade flows (e.g. sudden pivots into high-value pharma exports) indicate illicit activity, as summarized in Financial Crime Academy’s TBML vulnerabilities overview. One FATF case noted an IT company that abruptly began bulk pharmaceutical trading, a red flag for possible TBML using fake invoices or mispriced drug shipments (Financial Crime Academy’s TBML vulnerabilities overview). Complex payment chains involving third-party intermediaries disconnected from the healthcare business raise further alarms, including third-party payment red flags. Meanwhile, OFAC has penalized pharma-related entities for sanctions violations, such as the 2019 designation of an Argentina-based online pharmacy network “Goldpharma” as a narcotics trafficking and money laundering organization, per Treasury’s Goldpharma designation press release. These examples show that pharma and telehealth payment networks can inadvertently channel funds for sanctioned regimes or criminal cartels unless robust screening and due diligence are in place. Even INTERPOL has warned that pharmaceutical counterfeiting and illicit medical trade are “deeply tied to…money laundering” operations by organized crime, as noted in INTERPOL’s operation update.

In short, 2025 delivered a wake-up call: healthcare payments, from insurance claims to telemedicine fees and drug supply chains, are being hijacked by bad actors to wash money globally. Compliance leaders at billing platforms, payment processors, and health-focused fintechs should respond by urgently identifying and fixing the key AML risk surfaces in their systems. Below, we break down those risk areas and the practical steps (including new technologies) to address them.

Key AML Risk Surfaces in Healthcare Payment Platforms

Healthcare financial flows have some unique vulnerabilities that criminals are exploiting. By understanding these risk surfaces, platforms can target their AML improvements where it matters most. Major areas of concern include:

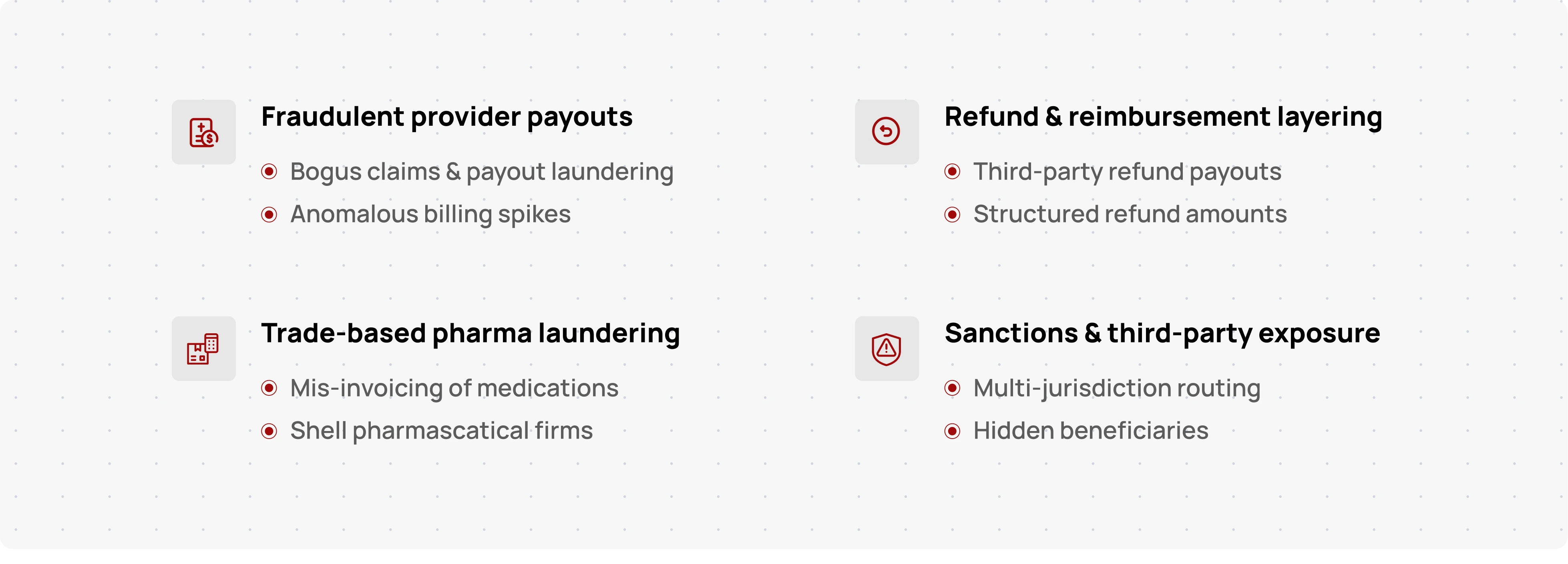

- Fraudulent Provider Payouts & Laundered Claims: Fraud rings often create fake clinics or corrupt providers to submit bogus claims (e.g. for unnecessary tests or phantom patients). Once payments are issued, the money is quickly layered through accounts and assets to obscure its origin (DOJ’s National Health Care Fraud Takedown announcement). For instance, a scam billing Medicare for expensive durable medical equipment might route the insurer’s payment to a shell medical supplier, then immediately transfer funds to offshore accounts or crypto wallets. These payout schemes combine traditional health care fraud with sophisticated laundering. Red flag: A healthcare provider that bills far beyond peers or shows sudden spikes in payment volume, followed by rapid withdrawals or transfers to unrelated entities. (In the DOJ takedown, analytics teams caught “anomalous billing” patterns by comparing providers (DOJ’s National Health Care Fraud Takedown announcement).)

- Refund & Reimbursement “Layering” Schemes: Refund processes in health payments (e.g. reimbursements to patients, credit balances, or claim overpayment refunds) can be manipulated as a laundering mechanism. Criminals may intentionally overpay or create fake transactions and then request large refunds to different accounts, effectively “cashing out” illicit funds under the guise of a refund. Refund scams in other industries have been linked to money laundering tactics, as described in Bitsight’s breakdown of refund fraud mechanics, and the concept extends here. Red flag: Unusual refund activity such as frequent refunds just under review thresholds, refunds issued to third-party payees rather than the original payer, or excessive refund requests tied to one provider or customer. These patterns can indicate an attempt to use the refund system to circulate illicit money. As one cybersecurity analysis noted, refund scams can involve “psychological manipulation and money laundering, not just product returns,” and are hard to detect without dedicated transaction monitoring.

- Trade-Based Laundering via Pharma Supply Chains: International pharmaceutical and medical supply payments are vulnerable to TBML schemes. This can involve mis-invoicing, over-valuing or under-valuing shipments, and using third-party distributor payments to mask money movements. A healthcare distributor might, for example, import a batch of medications at an inflated price from a foreign shell company, effectively sending excess value abroad (laundering funds) under cover of a legitimate trade invoice. FATF and Egmont have flagged scenarios like companies that suddenly expand into unrelated sectors like pharmaceuticals or engage in high-volume trades that don’t fit their profile (Financial Crime Academy’s TBML vulnerabilities overview). Red flag: Discrepancies between shipping documents and payments (e.g. paying far above market price for generic drugs), involvement of shell import/export firms with little business history, or routing payments through multiple jurisdictions without a clear business need. Close attention should be paid to cross-border pharma transactions, especially those involving high-risk regions, as they may also expose firms to sanctions breaches if any party is blacklisted.

- Sanctions Exposure and Third-Party Payment Networks: Healthcare and pharma payments can inadvertently entangle sanctioned individuals or entities, for example, a sanctioned country’s hospitals obtaining equipment via intermediaries, or narcotics traffickers using front companies to sell medical supplies. The complexity of healthcare supply chains (with group purchasing organizations, wholesalers, overseas shippers, etc.) means funds might pass through third-party accounts that obscure who the ultimate payer or beneficiary is. Criminal networks take advantage of this by inserting shell companies or money mules into the payment flow. Red flag: A payment path where the funding source or destination involves a party that isn’t clearly a healthcare entity (e.g. consulting or trading firms unrelated to medicine in the chain of payment), or transactions involving countries with strict sanctions or AML deficiencies. Robust sanctions screening and knowing your customer’s customer (KYCC) in these extended networks is vital to catching issues. A real-world cautionary tale is the Goldpharma case, where an online pharmacy network spanning several countries was found to be funneling opioid proceeds, leading to U.S. Treasury sanctions and asset freezes. No platform wants to discover belatedly that they processed payments tied to a sanctioned narcotics operation.

It’s evident that healthcare payment systems face a mosaic of financial crime risks, blending elements of fraud, trade-based schemes, and sanctions evasion. The good news is that healthcare organizations are allowed (and in fact encouraged) to use data analytics and information sharing to combat these threats. Despite the strict privacy regulations like HIPAA, there are clear carve-outs that permit anti-fraud and AML efforts.

Data Analytics Under HIPAA: Leveraging Patient Data to Fight Fraud & Laundering

One concern we often hear from healthcare payment processors is: “Are we even allowed to use patient data for AML and fraud analytics under HIPAA?” The answer is yes, not only allowed, but expected, as long as proper safeguards are in place. The HIPAA Privacy Rule classifies fraud detection and compliance activities as part of “health care operations,” which means covered entities (and their business associates) can use or share protected health information (PHI) for these purposes without individual authorization, per HHS’s HIPAA Privacy Rule overview and HHS’s definition of “health care operations”. In plain terms, if a hospital, insurer, or billing platform is analyzing PHI to detect billing anomalies, investigate fraud, or ensure compliance with laws, that is a permissible use under HIPAA.

Of course, HIPAA’s minimum necessary and security requirements still apply. Any analytics or monitoring must be conducted with strong access controls, role-based permissions, and audit logging of who accesses sensitive data. This is where having a purpose-built AML case management system becomes crucial. Such a system should, for example, allow a compliance analyst to review suspicious transactions involving PHI but log every access and action for audit purposes. It should also enable limiting what data fields are visible, to avoid unnecessary exposure of medical details. HIPAA explicitly requires organizations to implement audit controls to record and examine information system activity (e.g. access to electronic records). Embracing these principles, healthcare fintechs can confidently harness patient payment datasets for AML insights, identifying suspicious patterns while staying compliant with privacy laws. In fact, failing to monitor for fraud and abuse can carry its own regulatory risks, as HHS expects proactive compliance programs.

The takeaway: don’t let HIPAA be an excuse for blinders on financial crime. The law supports using patient billing and claims data to stop crime, as part of normal operations, so long as privacy protections are in place. With that green light, what practical steps and tools should healthcare payment platforms deploy? Let’s look at the must-fix areas and technology capabilities that can markedly improve AML defense.

Strengthening AML Controls in Healthcare Payments Platforms

Healthcare focused fintech platforms are now adopting advanced AML tech, from no-code rule builders to AI-driven anomaly detection, to spot and stop illicit activity in payment flows. Compliance teams should prioritize implementing the following controls and capabilities (which leading solution providers like Flagright are already offering):

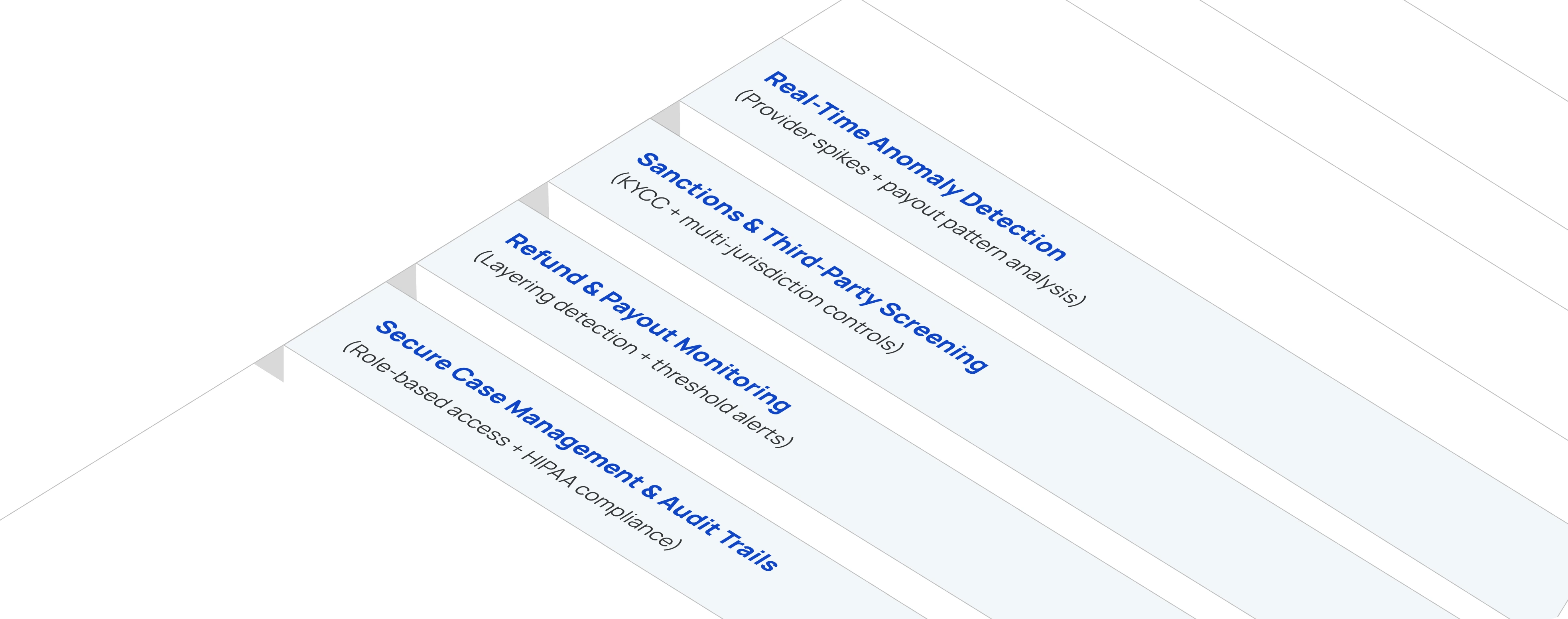

- Behavioral Analytics & Anomaly Detection: Given the dynamic nature of provider billing and patient payments, static thresholds alone won’t catch every scheme. Deploy machine learning and rule-based analytics to establish baselines for “normal” behavior (e.g. typical claim amounts per doctor specialty, usual refund frequency, normal cross-border payment volume for pharma shipments) and then flag deviations in real time. Modern AML platforms use anomaly detection to spot when a healthcare provider’s payout pattern suddenly shifts, or when a pharmacy’s disbursement volume spikes beyond statistical norms. These data-driven alerts can uncover schemes that evade simple rules. For example, in the DOJ takedown, it was data analytics detecting anomalous billing that helped uncover a $10B fraud ring before all funds went out (DOJ’s National Health Care Fraud Takedown announcement). By monitoring behavior drift, such as a clinic that usually processes $100k/month suddenly processing $1m with multiple international wire transfers, platforms can intervene early.

- Sanctions and Watchlist Screening on Payments: Every entity and account involved in a healthcare payment should be screened against up-to-date sanctions lists (OFAC, UN, EU), terrorist financier lists, and known bad actors (e.g. FDA debarment lists, INTERPOL notices on fake med sellers). This is especially critical for cross-border pharma payments or any third parties in the flow. Automated screening APIs can flag if, say, a medical supplier receiving funds appears on a sanctions list under a different alias, or if an address corresponds to a high-risk jurisdiction or an entity of concern. A robust AML system will screen not just at onboarding but continuously, including ad-hoc payees, refund recipients, or new vendor banks. The goal is to avoid scenarios like unknowingly facilitating payments to a front company of a cartel or a supplier in a sanctioned country. With the surge in fentanyl and opioid trafficking intersecting pharma supply chains, sanctions screening is non-negotiable; even FinCEN has highlighted how cartels exploit Chinese and Mexican shell companies in the healthcare context (Treasury’s FinCEN advisory on fentanyl-related illicit finance). Proactive screening protects your platform’s banking partners and keeps you off regulators’ radar.

- Targeted Rules for Refunds and Unusual Transactions: While machine learning adds intelligence, expert defined rules remain a cornerstone of AML, especially for known red flags. Healthcare payment processors should implement a set of specific rules, using a no-code rule engine if available, to catch high-risk patterns such as: a single patient ID getting multiple large refunds in a short period; a provider issuing refunds that exceed their charges (possible sign of laundering through credit balance refunds); or refunds going to accounts in a different name or country than the original payment source. Other useful rules might be: “alert if a claim payment is immediately followed by a withdrawal or transfer of most of the amount,” or “flag any disbursement to a shell company (no physical address or online presence)”. By configuring these scenarios, and testing them with historical data to fine-tune thresholds, compliance teams can quickly zero in on suspicious transactions. The key is having a flexible scenario builder that doesn’t require coding, so analysts can adapt rules as schemes evolve. For instance, if fraudsters start using partial refunds to avoid detection, the rules can be adjusted to flag multiple partial refunds adding up to large sums. Strong rule controls would likely have caught patterns in the refund scam example where a victim was tricked into sending back money, illustrating how transaction analysis can reveal anomalies (Bitsight’s breakdown of refund fraud mechanics).

- Secure Case Management with Audit Trails (HIPAA-Sensitive): When a suspicious transaction or pattern is identified, the next step is investigation , and this must be done in a secure, compliant manner due to the sensitivity of health data involved. A capable case management system should allow compliance investigators to dig into transaction details, link related alerts (e.g. multiple providers tied to the same bank account), and document their findings all within a protected environment. Role-based access is vital: for example, an investigator might see patient IDs or de-identified data, and only if further escalation is needed would specific patient information be revealed, and even then only to authorized personnel. Every access and action (viewing a record, attaching evidence, closing a case) should be logged. This not only satisfies HIPAA and internal security policies but also creates an auditable trail to demonstrate to regulators the thorough handling of each incident. Given the collaborative nature of healthcare fraud investigations (often involving payers, providers, and sometimes law enforcement), a good case management tool will also support controlled information sharing, such as exporting a redacted report of findings for law enforcement that omits unnecessary PHI. The bottom line: build an investigation process that is both effective and compliant, so that uncovering a money laundering scheme doesn’t inadvertently lead to a privacy violation. With audit-ready case logs and strict access controls, platforms can confidently partner with agencies like HHS-OIG or DOJ on follow-up investigations, knowing patient privacy remains intact.

By focusing on these areas, anomaly detection, sanctions screening, refund monitoring, and secure case handling, healthcare payment and billing platforms can significantly tighten their AML posture. It’s about marrying healthcare domain knowledge with proven fintech tools to close the gaps that criminals have been slipping through.

Turning AML Compliance into a Competitive Advantage

Far from being just a regulatory burden, strong AML controls can become a competitive differentiator for healthcare payment companies. Here’s why: First, demonstrating robust anti-fraud and anti-money laundering measures helps maintain and win crucial banking partnerships. Banks and payment processors are under increasing regulatory pressure to know their customers (KYB) and their customers’ compliance programs. A telehealth billing platform that can show it actively screens for illicit activity is far more attractive to bank partners (and less likely to face account closure or enhanced due diligence reviews) than one with a “see no evil” approach. Second, preventing fraud losses and laundering schemes at the outset directly saves money, every dollar stopped by an anomaly alert or a sanctions hit is a dollar that isn’t later written off or seized in an enforcement action. Over time, this strengthens the bottom line and lowers insurance and legal costs. Third, regulatory resilience: a company that can quickly provide auditors or regulators with a full audit trail of its compliance actions, that stays ahead of new advisories (be it a FinCEN notice or an HHS-OIG alert), will weather exams and inquiries with minimal disruption. This means management spends less time firefighting compliance issues and more time growing the business.

Finally, there’s a reputational angle. In an industry built on trust, patients trusting their insurers and payment platforms, pharmacies trusting their suppliers, being known as a secure and compliant operator builds brand value. Just as hospitals tout their patient safety standards, a healthcare fintech can market its financial integrity and partnership with authorities in safeguarding health dollars from crime. In a world of escalating healthcare scams, doing AML right signals that your platform is one that both customers and regulators can rely on.

In conclusion, the writing is on the wall: Healthcare payments must shed any remaining notion that AML is “someone else’s job.” Whether it’s a billing startup or a major claims processor, integrating strong AML controls is now an urgent product requirement. The threats, from laundered Medicare funds to illicit pharma trade, are real and growing. But with the right analytics, monitoring, and compliance framework, these platforms can not only meet the challenge but turn it into an advantage. By protecting the integrity of every transaction and ensuring no bad actors lurk in their payment flows, healthcare payment companies will safeguard their future in a heavily regulated landscape. It’s about fixing the vulnerabilities now, and in doing so, fortifying the trust and viability that their business depends on. The health of the financial system and the safety of patients’ funds deserve nothing less.