AT A GLANCE

Enterprises are replacing legacy, code-heavy AML systems with no-code AML platforms because the shift solves three problems at once: speed, accuracy, and accountability. No-code platforms cut implementation time from six to twelve months down to as little as two weeks, reduce false positives by as much as 93%, and give compliance teams direct control over detection logic without waiting on engineering resources. They also generate the audit trails and explainable outputs that regulators now expect from any modern AML program. This shift is not a fintech trend anymore. Banks, payment processors, and financial institutions of every size are adopting no-code AML infrastructure because legacy platforms simply cannot keep pace with today's transaction volumes, criminal typologies, or regulatory scrutiny.

What Problems Are Legacy AML Systems Creating for Enterprises?

Legacy AML systems create five recurring problems for enterprises: slow deployment, excessive false positives, poor agility, siloed data, and opaque AI models. Most legacy transaction monitoring platforms were built in the 2000s, long before real-time payments, crypto rails, and instant onboarding became standard. That architecture gap is why so many large institutions are now looking for alternatives.

Why Do Legacy AML Deployments Take So Long?

Legacy AML deployments take so long because every integration, rule change, or customization requires custom development work, often from outside consultants. Banks commonly report that rolling out a legacy transaction monitoring system takes six to twelve months or more, and even minor rule adjustments can require vendor support. That pace is difficult to justify when regulations and criminal tactics change far faster than a year-long IT project can accommodate.

Why Do Legacy Systems Generate So Many False Positives?

Legacy systems generate excessive false positives because they rely on static, threshold-based rules that cannot adapt to new transaction patterns. To avoid missing suspicious activity, institutions often set broad thresholds, which casts too wide a net. Industry estimates put false positive rates from traditional rule-based systems at 85% to 99%, with legacy engines like Actimize or Mantas cited as generating close to 90% false alerts. Adjusting those rules to be more precise is slow. Each tweak can take weeks of engineering and testing, and every change carries the risk of misconfiguration.

Why Are Legacy Platforms Slow to Respond to New Risks?

Legacy platforms are slow to respond to new risks because heavy coding and tuning requirements discourage teams from making changes. When an institution launches a new product line or encounters a novel money laundering scheme, updating monitoring rules becomes a major undertaking. Compliance teams often avoid touching legacy rules altogether because the process is risky and cumbersome, which leaves the institution a step behind evolving typologies.

How Do Siloed Systems Create Audit Gaps?

Siloed systems create audit gaps because fragmented tools make it difficult to maintain a unified view of risk. It is common for an enterprise to run separate systems for bank transfers, crypto transactions, and case management, which means an alert in one channel may not correlate with related activity in another. Many legacy systems also lack robust change management, so rule changes are not tracked with detailed version history or approvals, leaving it unclear who adjusted a scenario or whether it was properly tested.

Why Are Black-Box AI Models a Compliance Risk?

Black-box AI models are a compliance risk because they flag transactions without explaining the reasoning behind the decision. Some institutions have bolted machine learning modules onto legacy monitoring systems, but if an alert comes from an inscrutable algorithm, compliance teams cannot easily justify why it was flagged. Regulators and internal risk committees are increasingly wary of AI they cannot interrogate, which puts institutions in a difficult position: rely on rules that are transparent but brittle, or use AI that is effective but opaque.

Why Are Banks Moving Away From Legacy Platforms Like Oracle FCCM Toward Modular, API-First AML Systems?

Banks are moving away from monolithic legacy platforms toward modular, API-first AML systems because on-premise, heavily customized architectures are expensive to run and slow to change. Systems built on older architecture typically require dedicated infrastructure, lengthy implementation cycles, and specialized consultants for even routine configuration changes. Modular, API-first platforms take a different approach. Because they are cloud-native, they connect to core banking, payment, and case management systems through pre-built APIs instead of custom integration work, which shortens implementation timelines significantly and lowers the ongoing cost of maintaining the system. For enterprises weighing a migration, the appeal is straightforward: API-first platforms can be configured, tested, and scaled without the multi-year replatforming projects that older monolithic systems typically require.

What Do Regulators Expect From Modern AML Programs?

Regulators expect modern AML programs to be real-time, risk-based, and explainable, not static or opaque. Global bodies such as the Financial Action Task Force, along with national regulators including FinCEN, the Monetary Authority of Singapore, and the European Central Bank, have made clear that best-in-class AML programs need continuous, risk-based controls and documented, defensible decision-making.

Why Do Regulators Reject a Set-and-Forget Approach?

Regulators reject a set-and-forget approach because a rule set that never changes cannot keep pace with evolving typologies. U.S. regulators now expect a continuous risk-based approach, and an AML team that leaves its scenarios untouched for long stretches risks falling short of supervisory expectations. Compliance programs are expected to be dynamic, with frequent tuning as risks evolve.

What Does Explainability Mean for an AML Program?

Explainability means an institution must be able to show not just what its systems flag, but why. The Office of the Comptroller of the Currency and other regulators have issued model risk management guidance that stresses transparency in how detection models work. In practice, that means compliance officers must be able to clearly explain why a particular alert was generated or why a customer was scored as high-risk, which is difficult to do with opaque, unexplainable AI.

What Kind of Audit Trail Do Regulators Expect?

Regulators expect a documented audit trail for every change made to an AML system. If a bank updates its transaction monitoring scenario, examiners want evidence that the change was vetted, tested, approved, and recorded, including who made the change and when. This is often described as scenario governance, and it applies to every parameter change or new rule added to the system.

No-code AML platforms align closely with these expectations because they let institutions move quickly while automatically recording every change and its justification. Built-in version control, approval workflows, and one-click audit reporting make it far easier to satisfy a regulator's request for traceability, which is a major reason enterprises are gravitating toward no-code solutions.

How Much Time and Money Can No-Code AML Platforms Save?

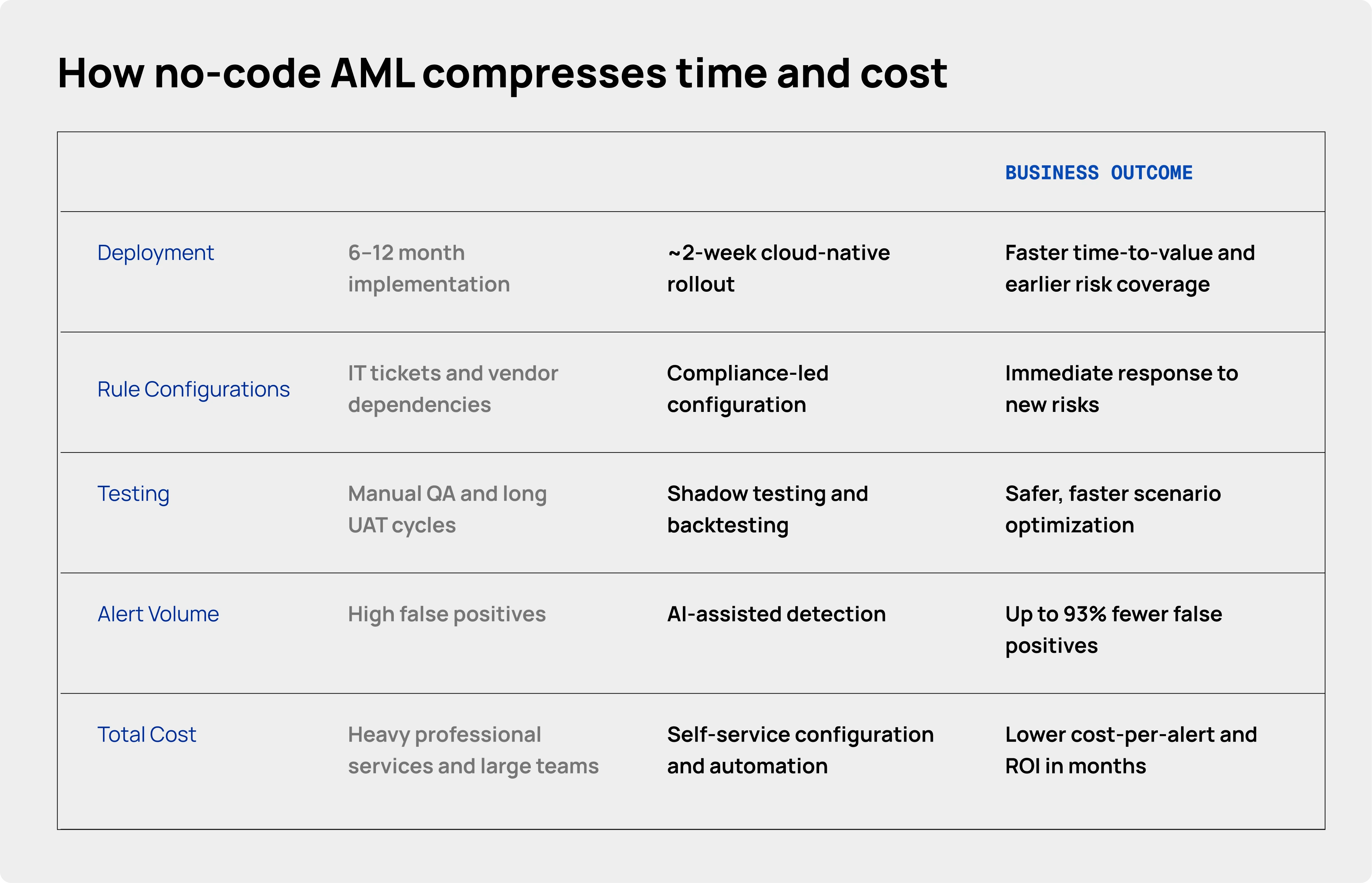

No-code AML platforms typically cut deployment time from months to weeks and can reduce false positive volumes by up to 93%, which translates directly into lower operational costs and faster time to compliance.

How Fast Can an Enterprise AML Platform Actually Be Implemented?

An enterprise AML platform can realistically be implemented in as little as two weeks when it is cloud-native and API-first. Case studies show that many clients integrate Flagright's platform in about two weeks, compared to the six to twelve month timelines typical of legacy systems. There is no need to provision on-premise hardware or run lengthy data mapping exercises, since the vendor handles most of the integration work through pre-built connectors. For enterprises evaluating implementation partners and asking whether a 90-day rollout is realistic, the answer with a modern no-code platform is usually yes, and often faster, depending on the complexity of existing data sources and the number of integrations required.

What Is the Total Cost of Ownership Compared to Legacy Systems?

The total cost of ownership for a no-code AML platform is typically lower than legacy systems because it eliminates most professional services fees, hardware costs, and version upgrade cycles. Legacy vendors and platforms with heavy customization requirements, similar to older engines like ThetaRay's earlier deployments or other on-premise systems, generally require ongoing consulting engagements just to keep rules current. No-code platforms move that configuration work in-house, since compliance teams can make changes themselves through the interface. One Flagright customer case study reported full ROI in under five months, driven by faster deployment, fewer false positives, and less reliance on outside specialists.

Does No-Code Reduce Dependence on IT and Engineering Teams?

Yes, no-code AML platforms significantly reduce dependence on IT and engineering resources because rules and workflows are configured through dashboards rather than code. One Flagright user reported being able to tweak scenarios in response to new risks without waiting weeks for vendor support. That self-service capability means the organization can respond to suspicious trends immediately, and it also lowers cost, since banks avoid the professional service fees legacy vendors charge for every customization.

Quick Tip: How to Evaluate Implementation Timelines

- Ask vendors for a reference client with a similar transaction volume and ask how long their actual go-live took, not the marketed estimate.

- Confirm whether rule changes after go-live require vendor involvement or can be made in-house.

- Check whether the platform supports shadow mode testing before rules go live, which shortens the tuning period significantly.

In short, no-code AML platforms let institutions move faster, adapt easier, and run leaner. They replace the brittle, slow legacy approach with one that is agile and cost-effective by design. Next, we’ll look at some key capabilities that enable these benefits, and how they work in practice.

What Key Capabilities Should a Modern No-Code AML Platform Have?

A modern no-code AML platform should include a visual rule builder, version-controlled governance, built-in testing tools, and integrated case management. These four capabilities directly address the speed, accuracy, and audit gaps found in legacy systems.

What Does a No-Code Rule Builder Actually Do?

A no-code rule builder lets compliance officers create and modify detection rules through a visual interface instead of writing code. Users select conditions and thresholds from menus, connect logic blocks, and build custom scenarios using customer attributes, transaction patterns, and behavioral metrics. Flagright's platform, for example, allows teams to create custom scenarios in minutes through an interface that requires no engineering help. Because a new rule can be deployed in minutes instead of weeks, compliance teams can respond immediately when a new money laundering scheme or regulatory requirement emerges.

How Does Version Control Support Governance?

Version control supports governance by automatically tracking every change made to a scenario or model, including who made the change, when, and why. Enterprise-grade no-code platforms typically require a manager to review and approve changes before they go live, known as a maker-checker control, which prevents any single individual from introducing risky changes without oversight. Teams can also roll back to a previous version if a change does not perform as expected, which removes the fear that adjusting the system might break compliance.

Why Do Testing and Simulation Tools Matter Before a Rule Goes Live?

Testing and simulation tools matter because they let teams validate a new rule's effectiveness before it affects real alerts. Shadow mode allows a proposed rule to run in parallel with live transactions, logging what it would have triggered without generating real alerts. Historical backtesting lets teams replay past data through a new rule to see how many alerts it would have produced and whether it would have caught previously missed cases. A platform might show, for example, that a new scenario would reduce false positives by 30% over the last three months while still catching every true case, which removes the guesswork from rule tuning.

Why Does Integrated Case Management Matter for Enterprise AML Programs?

Integrated case management matters because it eliminates the data silos that slow down investigations and weaken audit trails. When transaction monitoring, customer risk scoring, watchlist screening, and case management run on one platform, an alert flows directly into a case that is already linked to the relevant customer profile and KYC information. Investigators work from a single dashboard instead of switching between disconnected systems, and every action taken during an investigation, from initial review to SAR filing, is logged and time-stamped automatically.

.webp)

How Does Flagright Put No-Code AML Capabilities Into Practice?

Flagright is an AI-native, unified AML compliance platform that combines real-time transaction monitoring, explainable AI, and integrated case management into a single no-code system built for enterprise scale.

How Fast Is Flagright's Transaction Monitoring in Practice?

Flagright's transaction monitoring engine screens transactions in real time, with sub-second response times and 99.99% uptime, even at high volumes. Transactions are ingested through a single API and screened as they occur, whether the payment is a SWIFT wire transfer or a crypto transaction on the blockchain. Risk-based customization is built into the no-code scenario builder, so teams can apply stricter thresholds to higher-risk geographies or customer segments without slowing down monitoring for lower-risk activity.

How Does Flagright Avoid the Black-Box AI Problem?

Flagright avoids the black-box AI problem by making every AI-driven insight explainable by design. Its AI Forensics module assigns risk scores and prioritizes cases, but it always provides the reasoning behind that score, for example, flagging that a transaction volume is five times higher than usual for a customer and that the counterparty is in a high-risk country. Every action the AI takes is logged in the case timeline, so investigators and regulators see the outcome and the rationale behind it. Final decisions remain with human analysts, with the AI acting as a transparent recommendation engine rather than an unexplainable filter.

How Does Flagright Handle Case Management and Audit Trails?

Flagright handles case management and audit trails by keeping the entire AML lifecycle in one system, from transaction monitoring through investigation to SAR filing. Every step of a case is logged automatically, including who investigated it, what notes were added, and when it was closed. Compliance officers can pull a comprehensive report of all alerts and actions for a given period in a single click, which makes the program audit-ready at every stage rather than only during examination periods.

Can Flagright Scale to Enterprise Transaction Volumes?

Yes, Flagright is built to scale horizontally and handle tens of millions of transactions per day without performance degradation. The platform maintains bank-grade security standards and has been validated through a partnership with the London Stock Exchange Group. Banks, fintech companies, and payment processors across six continents use the platform, and clients have reported user adoption rates above 95%, which matters because a compliance tool only delivers value if analysts actually use it correctly.

How Does Flagright Compare to Other AML Platforms Like Unit21?

Flagright and Unit21 both offer no-code rule building and case management, but they differ in scope and architecture. Unit21 built its reputation primarily around fraud and risk case management workflows, while Flagright was designed from the ground up as a unified AML compliance platform that combines real-time transaction monitoring, sanctions screening, dynamic risk scoring, case management, and explainable AI forensics in one system. For enterprises comparing the two, the practical difference usually comes down to how much of the AML lifecycle needs to live on a single platform versus being stitched together from multiple point solutions. Institutions that want transaction monitoring, KYC risk scoring, and investigation tools unified under one no-code interface, with an AI layer that explains its own reasoning, tend to find that consolidation reduces both cost and audit complexity compared to running separate best-of-breed tools.

Quick Tip: What to Ask When Comparing AML Vendors

- Ask whether transaction monitoring, case management, and sanctions screening run on one platform or require separate integrations.

- Request a side-by-side false positive reduction benchmark using your own historical transaction data, not a generic industry average.

- Confirm how the vendor's AI explains its risk scores, and ask to see an example case timeline before signing a contract.

The Bottom Line on No-Code AML Adoption

No-code AML platforms have moved from a fintech convenience to an enterprise standard. Large banks and financial institutions are adopting them because the complexity of financial crime is growing while regulatory expectations keep rising, and legacy systems simply were not built to keep pace with either. By switching to no-code platforms, enterprises can deploy new controls in days instead of quarters, respond to emerging threats proactively, and cut the operational noise and labor tied to compliance work. In one documented case, consolidating siloed legacy systems into a unified no-code platform reduced false positives by 93%, freeing compliance teams to focus on genuine risk instead of chasing false alarms. As payments get faster and criminal tactics keep adapting, the institutions that can iterate quickly and prove their decisions transparently will be the ones that stay ahead, rather than merely keeping up.

Frequently Asked Questions

What is the difference between crypto compliance software and traditional AML systems?

Crypto compliance software is built to monitor blockchain-native activity, including wallet addresses, on-chain transaction flows, and token transfers, while traditional AML systems were designed around bank transfers, card payments, and fiat rails. Many enterprises now need both types of coverage in one platform, since customers move funds across fiat and crypto channels interchangeably. A modern no-code AML platform that supports both transaction types avoids the need to run separate, disconnected monitoring systems for each.

How does open-source transaction monitoring software compare to traditional AML vendors?

Open-source transaction monitoring software offers more flexibility and no licensing fees, but it typically requires an in-house engineering team to build, maintain, and update detection logic, which shifts the cost from software fees to internal development resources. Traditional AML vendors provide a managed, supported product but often come with the same slow deployment and rigid rule limitations found in legacy systems. No-code platforms sit between the two, offering vendor-supported infrastructure with the flexibility to configure and change detection logic without writing custom code.

What does cost per alert mean in AML transaction monitoring, and why does it matter?

Cost per alert measures the total operational cost of investigating a single alert, including analyst time, tooling, and overhead, divided by the number of alerts generated. It matters because a high false positive rate inflates this figure significantly, since analysts spend time investigating alerts that turn out to be benign. Reducing false positives through smarter, AI-assisted detection directly lowers cost per alert, which is one of the clearest financial metrics enterprises use to justify switching platforms.

How do no-code KYC tools reduce time-to-market for new compliance programs?

No-code KYC tools reduce time-to-market by letting compliance teams configure onboarding workflows, risk scoring logic, and verification requirements through a visual interface instead of waiting on development cycles. A new product line or market entry that once required months of custom KYC integration work can often be configured and tested in days, since the underlying platform already supports the necessary identity verification and risk assessment building blocks.

Can no-code tools adapt KYC flows to different customer risk levels?

Yes, no-code platforms typically allow compliance teams to configure different verification requirements and monitoring intensity based on a customer's risk tier. A low-risk retail customer might go through a streamlined verification flow, while a high-risk customer in a higher-risk jurisdiction can be routed through enhanced due diligence steps automatically, all configured through the same no-code interface without separate custom builds for each risk tier.

Is no-code AML technology secure enough for large, regulated enterprises?

Yes, enterprise-grade no-code AML platforms are built to bank-grade security standards, including encryption, role-based access controls, and independent validation. No-code refers to how compliance teams configure detection logic, not a reduction in the platform's underlying security or infrastructure. Institutions evaluating a no-code vendor should still confirm certifications, uptime guarantees, and data residency options, the same due diligence applied to any enterprise software purchase.

Do no-code AML platforms work for smaller compliance teams, not just large banks?

Yes, no-code AML platforms are particularly well suited to fintechs and smaller compliance teams because they remove the need to hire dedicated engineers just to maintain the monitoring system. A lean compliance team can configure, test, and adjust detection rules directly, which allows a smaller organization to run an AML program with the same rigor as a much larger institution, without the corresponding headcount.

What real-world problems have enterprises actually solved using no-code AML platforms?

Enterprises using no-code AML platforms have documented reductions in false positive alerts of up to 93%, implementation timelines shortened from six to twelve months down to about two weeks, and full ROI achieved in under five months in at least one case study. Beyond the numbers, institutions report that compliance teams can now respond to new money laundering typologies within days instead of waiting on lengthy vendor change requests, which was previously one of the biggest operational gaps in legacy AML programs.