Chargebacks are draining over $33 billion globally and rising fast. Payment processors must confront new network rules, surging friendly fraud, and regional spikes head-on. This piece challenges PSPs to reframe chargebacks not as a cost of doing business but as a strategic inflection point, backed by global data, sharper risk analysis, and a call to action for proactive dispute management.

The Costly ‘Cost of Doing Business’

Chargebacks; the dreaded transaction disputes that reverse payments, have long been shrugged off by some payment service providers (PSPs) as an inevitable cost of doing business. That complacency is no longer tenable. Global chargeback losses are soaring to unprecedented levels, projected to reach $33.79 billion in 2025 and climbing to $41.69 billion by 2028. To put it bluntly, in just three years the financial impact of chargebacks is set to jump over 23%, a surge that should make any PSP executive’s stomach drop. Recent studies even peg merchant losses from chargebacks at around $117.5 billion in 2023 alone when you tally up lost sales, fees, penalties, and overhead.

Yet the true shocker for PSPs is how fundamentally the chargeback landscape is shifting. New card network rules are tightening the screws on allowable dispute rates, “friendly fraud” now accounts for roughly 70-75% of all chargebacks, and regions that once saw modest dispute activity are now hotbeds of growth. If you’re a PSP leader reading this, it’s time to cast aside any rose-colored notion that chargebacks are a back-office nuisance. Instead, start seeing them for what they are: a strategic risk and a barometer of your business’s health. This article will delve into the hard numbers, global trends, and scheme rule changes forcing a paradigm shift and argue why PSPs must radically reframe how they think about and manage chargebacks.

The Rising Tide: Global Chargeback Trends (2023–2025)

Chargebacks are spiking worldwide. What used to be a trickle of disputes has swelled into a flood as e-commerce and digital payments proliferate. In 2023, there were an estimated 238 million chargebacks globally. By the end of 2025 that number is forecasted to approach 265-270 million, on pace to hit ~337 million by 2026, a staggering 40%+ increase in just a few years. Put another way, the “chargeback economy” (if we dare call it that) is expanding faster than overall payment volumes. Mastercard’s analysts project a 24% jump in dispute volumes from 2025 to 2028, reaching about 324 million annual chargebacks by 2028. No region is immune: North America may lead in dispute counts today, but the rest of the world is catching up fast (as we’ll explore later).

Why this surge? In large part, the growth in digital transactions has opened the floodgates. More online purchases, especially card-not-present (CNP) transactions, inevitably mean more opportunities for disputes. Cardholders often fail to recognize legitimate online charges or encounter unfamiliar merchant names, leading them to initiate chargebacks for transactions they actually did authorize. A simple UX detail, like a confusing billing descriptor, can convert a routine purchase into a dispute. Additionally, the subscription economy’s rise has contributed to dispute volume, as customers grapple with managing recurring charges, many disputes stem from “I forgot to cancel” or confusion over subscription renewals.

However, the biggest driver isn’t just transaction growth; it’s fraud, especially so-called friendly fraud. Industry data indicate that around 70-75% of chargebacks are now linked to “friendly” or first-party fraud. This means the customer (or someone in their household) actually made the purchase, but later disputes it, often citing reasons like “item not received” or “unauthorized” even when that’s not true. Some of this is outright cyber-shoplifting; some is legit confusion or buyer’s remorse. Either way, it’s become the single biggest factor behind disputes. Traditional third-party fraud (where a stolen card is used) is still a major issue, global CNP fraud losses are estimated to hit $28.1 billion by 2026, but increasingly it’s legitimate cardholders driving the chargeback spike. In fact, one report found first-party (friendly) fraud now represents 36% of all fraud claims globally, up from just 15% a year prior, showing how sharply consumer behavior has shifted.

Meanwhile, consumer attitudes and behaviors are fanning the flames of disputes. Surveys show that a whopping 81% of customers file a chargeback because it’s simply more convenient than contacting the merchant for a refund. With banks rolling out one-click dispute buttons in mobile apps, it’s no surprise that ease of filing has led to 30-40% higher dispute volumes in markets like the U.S. where self-service filing is available. The process has become so frictionless that many buyers treat chargebacks as an alternative customer service channel. In fact, 72% of consumers in one survey didn’t grasp the difference between a chargeback and a standard refund, viewing chargebacks as just another way to “get my money back.” The result? Disputes are often triggered at the first sign of dissatisfaction, without giving the merchant a chance to resolve the issue. Little wonder that over half of cardholders (around 52-53%) now go straight to their bank, bypassing the merchant, when they have a payment issue. This all creates a perfect storm where chargeback volumes aren’t just rising in tandem with sales but also outpacing them.

For PSPs, these trends should set off alarm bells. More chargebacks across the board mean more pain for the entire payments ecosystem. Processors and acquiring banks ultimately bear the brunt of excessive disputes through scheme fines, increased compliance scrutiny, and deteriorating merchant portfolios. No corner of the globe is safe either. Regions like Latin America and Asia-Pacific, once relatively low-dispute markets, are now seeing the fastest acceleration (double-digit annual increases) in chargebacks as eCommerce booms. We’ll dig into regional specifics shortly, but the big picture is clear: the chargeback wave is rising worldwide, and PSPs need to brace themselves with data-driven strategies.

The True Cost: Beyond Lost Transactions

If the volume trends are alarming, the economics behind chargebacks are even more so. Many PSP executives have historically viewed a chargeback as roughly “the cost of the sale plus a $15 fee.” In reality, the downstream costs cascade far beyond that, for merchants, for acquirers, and for the broader ecosystem. Let’s break down the full economic burden of a chargeback, which includes direct losses, fees, operational overhead, and hidden opportunity costs.

- Direct Financial Losses: At its most basic, a chargeback forces the merchant to refund the sale amount (or the acquirer to credit the cardholder and later claw it from the merchant). If a product was already shipped or a service rendered, that revenue is gone. Worse, the merchandise cost is often lost too, especially for physical goods that the merchant may never recover. Studies show businesses effectively lose $3.75 to $4.60 for every $1 in chargeback transactions once you factor in product cost, shipping, marketing, and overhead. U.S. merchants in particular are estimated to be incurring $4.61 in total costs per dollar of fraud in 2025, a sharp increase of 37% from just a few years ago. In other words, chargebacks don’t just reverse a sale, they multiply the loss.

- Bank and Network Fees: On top of the lost sale, there are the explicit fees. Card networks charge acquirers and merchants non-negotiable chargeback fees (often $15-$25 per incident) regardless of whether the dispute is ultimately won or lost by the merchant. These add up fast. If a merchant faces 1,000 chargebacks a month, they might burn tens of thousands of dollars just in fees. And if the merchant’s chargeback ratio creeps too high, additional fines or “compliance fees” kick in (often $100+ per dispute in penalty) as we’ll discuss in the section on compliance programs. A table comparing typical fee structures could illustrate how, for example, a friendly fraud chargeback might cost a $100 product + $20 fee + higher future processing costs, versus a legitimate refund which would have just been the $100. The bottom line: a chargeback turns a sale into a significant net loss.

- Operational & Overhead Costs: Perhaps the most underappreciated cost is the manpower and technology required to manage disputes. Financial institutions on average spend about $9-$10 to process a single chargeback through their systems. That figure includes the army of back-office staff, call center agents, and fraud analysts needed to handle the paperwork and investigation. In fact, U.S. banks must hire roughly one full-time employee per ~$13,000 in annual chargeback volume to keep up. For a mid-sized issuer or acquirer dealing with say $50 million in disputed transactions a year, that translates to hundreds of full-time staff dedicated purely to the chargeback process. PSPs ultimately pass some of these costs to merchants via higher discount rates or reserve requirements, but there’s no denying it erodes margins across the board. Merchants, for their part, also incur internal labor costs, dealing with disputes is time-consuming. Many large merchants now maintain entire chargeback departments. Half of merchants (50%) handle chargebacks completely in-house, bearing all those salary costs, while about 34% outsource dispute handling to specialized firms (often on a contingency fee basis) and only 16% outsource everything (fraud and chargebacks). There’s no free lunch: whether done internally or via vendors, someone is paying for all those analysts piecing together evidence to contest chargebacks.

- Technology & Tools: As chargeback volumes grew, so too did the cottage industry of chargeback prevention and management tools. Merchants report spending anywhere from $100,000 to $500,000 annually on chargeback management technology, from alert systems to case management software to AI-driven fraud filters. Not to mention the integration and maintenance costs that come with these systems. Notably, 12% of large enterprises said their chargeback tech costs jumped over 25% in the past year, illustrating how fighting disputes is becoming more complex (and expensive). PSPs themselves invest heavily in risk monitoring systems to flag high-risk transactions and to interface with network alert programs. All these tools are necessary, but they add another layer to the total economic impact of chargebacks.

- Intangible Costs (Reputation & Relationship Damage): Beyond dollars and cents, consider the reputational hit. Excessive chargebacks label a merchant (and by extension, its PSP/acquirer) as “high-risk.” This can strain the relationship with acquiring banks and card networks, no one wants to be the bank servicing the worst-offending merchants. Acquirers might respond by holding a reserve of the merchant’s funds (tying up cash flow) or even outright terminating the merchant account if things get out of hand. From the merchant’s perspective, a chargeback also often means a lost customer; a cardholder who files a dispute is unlikely to shop with that merchant again. And in cases of friendly fraud, it might even be a good customer that’s now effectively “fired” due to being blocked by fraud systems after a chargeback. These opportunity costs, lost future sales, damaged customer relationships, and tarnished bank partnerships, are harder to quantify but painfully real.

In aggregate, when you add it all up, it’s clear that the true cost of chargebacks is magnitudes higher than the transaction value itself. For PSPs, this has a direct impact on economics: higher operational expenses, more resources on compliance, and the risk of merchant attrition or fines. It’s sobering to realize that merchants only win about 45% of the chargebacks they fight on averagepaycompass.com, meaning more than half of disputes result in money permanently out the door along with all those added costs. And that merchant win-rate hasn’t budged much in years, despite better tools, a testament to how tilted the chargeback system remains in favor of cardholders and issuers. The deck is stacked, and every dispute that escalates is likely money lost.

For PSPs, internalizing this full cost picture is crucial. It underscores why simply absorbing chargeback losses or passing fees to merchants is not a sustainable strategy. Instead, the economically sound approach is to prevent disputes or resolve them before they become chargebacks. A later section will explore how forward-thinking PSPs can do exactly that, turning dispute prevention into savings. But first, let’s examine a factor that’s about to make chargeback management even more challenging: the card networks’ tightening grip through new compliance programs.

Scheme Rule Shake-Up: VAMP, ECM, and the New Compliance Reality

If rising volumes and costs weren’t enough, 2025 is the year the card schemes (Visa and Mastercard) decided to rewrite the rules of the game. PSPs and acquirers are now grappling with sweeping changes to chargeback and fraud monitoring programs, changes that carry serious financial and operational implications. The Visa Acquirer Monitoring Program (VAMP) and Mastercard’s longstanding Excessive Chargeback programs (ECM/HECM) are at the center of this shake-up. Let’s break down what PSP leaders need to know:

Visa’s VAMP; A New Era of Consolidated Compliance: In April 2025, Visa rolled out the Visa Acquirer Monitoring Program (VAMP), a major overhaul that consolidated five existing fraud and dispute monitoring programs into one. Instead of juggling separate thresholds for fraud (like TC40 counts) and chargebacks, Visa now uses a single combined metric to flag problem accounts. Crucially, VAMP doesn’t just target merchants, as the name implies, it holds acquirers (and their PSP agents) accountable for excessive dispute activity in their portfolio. Visa’s message is clear: if you, the PSP/acquirer, are boarding merchants with high fraud and chargeback rates, you will be on the hook.

The threshold dynamics under VAMP are a story in themselves. Initially, Visa communicated that merchants (and their acquirers) would be flagged as “Excessive” if disputes exceeded roughly 1.5% of sales under the old regime. But with VAMP’s combined fraud+dispute formula, Visa temporarily raised the threshold to 2.2% in mid-2025 to avoid an avalanche of merchants being flagged right away. This gave a bit of breathing room as everyone adjusted to the new math. However, that leniency is short-lived. Visa has announced that from April 2026, the Excessive dispute threshold will ratchet down to about 0.9%. Yes, you read that correctly, under 1%. That is a drastic tightening, effectively cutting the acceptable dispute ratio by more than half. It means even today, merchants are being warned to keep their chargeback ratios well below 1% if they want to avoid triggering alarms. For PSPs, this is huge: many industries historically operate comfortably around 0.5-1% dispute rate; now even 0.9% will be considered too high come 2026. A timeline chart of these VAMP threshold changes (from ~1.5% to 2.2% to 0.9% within a year) would vividly illustrate how rapidly the noose is tightening on dispute tolerance.

Beyond just ratios, VAMP consolidates fraud reports and chargebacks into one program. Notably, under VAMP rules fraud reports that later become chargebacks are essentially counted twice against the threshold. This is a crucial detail: it means merchants (and thus acquirers) can’t ignore fraud alerts thinking “at least it hasn’t charged back yet”, in VAMP, that eventual chargeback will worsen your ratio in addition to the fraud incident itself. The idea is to push acquirers to intervene on fraud before disputes happen. Practically, PSPs will need to invest in better fraud monitoring and work more closely with merchants to address fraud red flags immediately, lest they get hit doubly in the stats.

Mastercard’s ECM/HECM; Still Going Strong (and Strict): Mastercard, for its part, has long had the Excessive Chargeback Program (ECP) which designates merchants as either Excessive Chargeback Merchant (ECM) or High Excessive Chargeback Merchant (HECM) depending on their dispute levels. These thresholds remain in play and are a bit more complex: to be tagged as an ECM, a merchant needs to have at least 100 chargebacks in a month AND a chargeback ratio above 1.5% (up to 2.99%). The “High” category, HECM, is for the worst offenders: 300 or more chargebacks in a month AND a ratio of 3% or higher. Both conditions; volume and ratio, must be breached, which is a slight philosophical difference from Visa (Visa will flag even a low-volume merchant if the ratio is high, whereas Mastercard wants to see a certain absolute count too). This means a small business with only 50 transactions but 3 chargebacks (6% ratio) wouldn’t trigger ECM because it didn’t hit 100 chargebacks total; conversely, a huge retailer with 500 chargebacks but a 0.5% ratio also wouldn’t trigger. But if you blow past both the volume and percentage thresholds, Mastercard will waste no time slapping the ECM/HECM label on.

The consequences of landing in Visa’s or Mastercard’s penalty box are severe. Under VAMP or ECP, once a merchant is formally in the program, the acquirer is notified and typically must work with the merchant on a remediation plan to get disputes down. Meanwhile, monthly fines kick in. Visa’s fines for excessive disputes can be on the order of ~$10 per chargeback in the early stages which might not sound huge, but multiply that by thousands of chargebacks and it stings (and Visa fines escalate for continued non-compliance). Mastercard’s fines are notoriously higher: ECM merchants can face thousands of dollars in fines each month, and HECM fines climb even higher, often exponentially with each passing month of non-compliance. It’s not unheard of for a merchant in HECM status to be fined tens of thousands per month, and those fines are usually charged to the acquirer, who will definitely pass them along or deduct from the merchant’s settlements.

Beyond network fines, PSPs may also impose their own safeguards: increased processing fees, rolling reserves, or even freezing payouts for merchants in these programs. All of this is to mitigate risk, but it can feel like death by a thousand cuts for the business involved. And if things don’t improve, the endgame is account termination: Mastercard, for example, makes it clear that HECM status can lead to the acquirer ceasing processing for that merchant. Visa similarly can demand acquirers drop a merchant who doesn’t get under control. From a PSP’s perspective, that means losing a client (and revenue) and possibly eating financial losses if the merchant goes out of business under the weight of chargebacks.

For PSP leaders, these scheme rule changes are a double-edged sword. On one side, they incentivize doing what we all agree is good, keeping fraud and disputes low. On the other, they add significant compliance risk and cost to managing a portfolio of merchants, especially in high-risk verticals. A savvy PSP now must proactively monitor merchants’ chargeback ratios in real time, effectively acting as a risk coach to clients. If a merchant starts trending towards the threshold (say 1% and rising), the PSP needs to step in before Visa or Mastercard does. This could involve anything from counseling the merchant on dispute prevention, requiring them to use fraud tools, or even freezing some of their funds to cover potential fines. It’s a more hands-on role for acquirers than ever before.

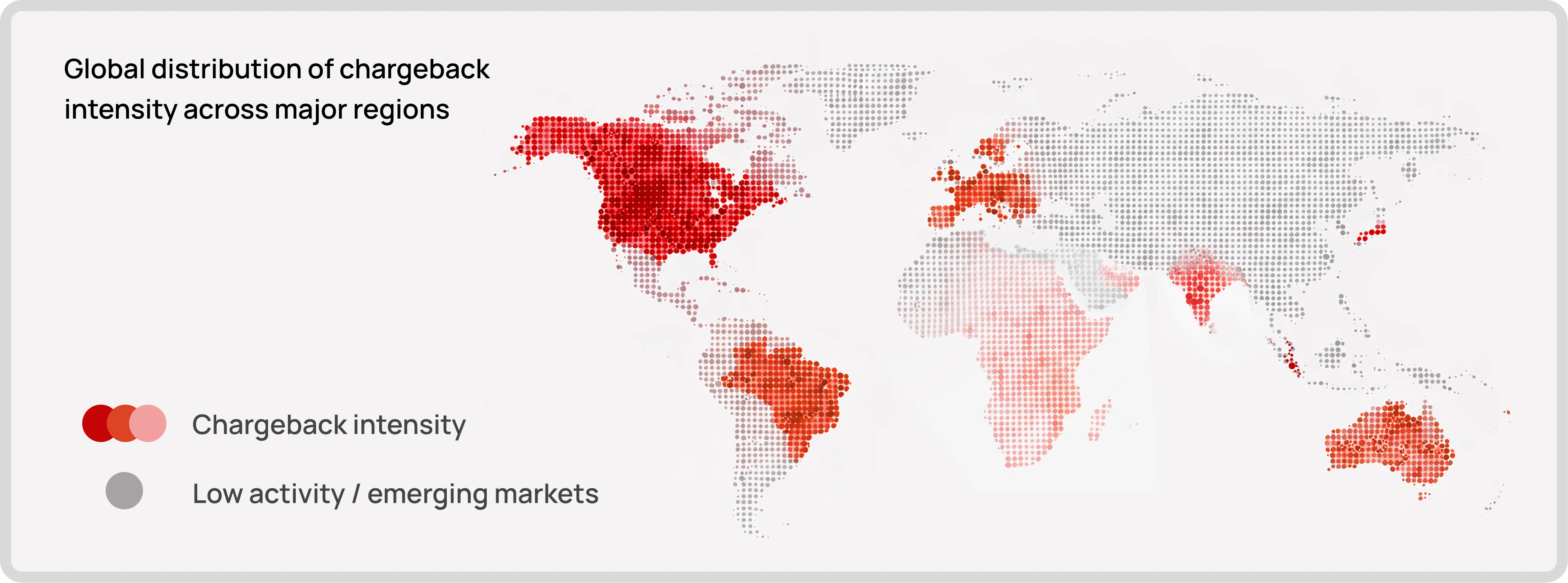

Global Perspectives: How Regions Stack Up

Chargebacks may be a global phenomenon, but the distribution and dynamics vary widely by region. PSPs operating internationally (or in specific markets like APAC or LatAm) need a nuanced understanding of these differences. Let’s take a tour of the world:

- North America (U.S. and Canada): The United States remains the epicenter of chargeback activity by sheer volume and value. U.S. merchants not only face the highest dispute counts, but also the highest average value per chargeback (around $110 per dispute, the highest of any country studied. This is likely due to higher average transaction values and a litigious consumer culture. By 2028, North America’s chargeback amounts are forecast to reach $20.5 billion, nearly half the global total. Canada, while smaller in population, follows similar patterns to the U.S. thanks to a shared credit card infrastructure and consumer behavior, though Canadian banks historically have slightly lower fraud rates. North America is the most mature market with established fraud prevention, yet ironically still leads in total chargebacks. One factor is the high adoption of digital banking and easy dispute filing (remember that 81% convenience stat). On the bright side, North America’s growth in chargeback volume is projected at a relatively modest 16% from 2025 to 2028, slower than elsewhere, perhaps because it’s already at high levels and also due to broader adoption of fraud controls like EMV, 3-D Secure, etc. Still, PSPs in the U.S. and Canada can’t be complacent: even stable chargeback volumes here mean tens of millions of disputes and billions in losses annually. Another notable aspect: U.S. regulators and consumer rights focus means chargeback rights are strongly enforced, merchants have few ways to reject a dispute outright, which keeps volumes high.

- Europe (EU and U.K.): Europe’s chargeback landscape has been shaped by regulation like PSD2’s Strong Customer Authentication (SCA). By forcing two-factor authentication on most online card transactions, the EU managed to significantly dent fraud rates on genuine unauthorized transactions. This is one reason Europe’s share of global chargeback costs is relatively small (projected around $3.17 billion by 2028), far lower than North America’s. Also, European consumers historically use alternative payment methods (like iDEAL, SEPA, etc.) for some online purchases, which have different dispute mechanisms, partially reducing card chargeback exposure. That said, friendly fraud is filling the gap. Some EU merchants report that while fraud declines due to SCA, overall disputes haven’t dropped as much, meaning more cardholders are disputing legitimate charges (perhaps out of frustration with SCA friction or simply a growing awareness of their chargeback rights). The U.K., no longer under EU’s PSD2, implemented its own strong auth requirements and sees similar trends. The average chargeback value in the U.K. is about $82, notably lower than the U.S., possibly reflecting smaller transaction sizes or quicker refund practices that keep smaller disputes out of the system. Europe’s chargeback volume is set to grow ~27% from 2025 to 2028 faster than North America’s growth, albeit from a lower base. European PSPs should particularly watch for an uptick in first-party fraud cases, likely because robust security measures have forced criminals and opportunistic consumers alike to exploit the chargeback process instead of traditional fraud.

- Latin America (LatAm): Latin America is experiencing an e-commerce renaissance, and with it, a wave of disputes. By 2028, LatAm’s chargeback losses are forecast around $8.5 billion. The region’s growth in chargeback volume (estimated ~22% from 2025 to 2028) outpaces North America’s. Why? A combination of rapidly growing online sales (more people transacting by card than ever) and historically higher fraud levels in some LatAm markets. In countries like Brazil, the largest LatAm economy, the average chargeback is about $94, not far behind the U.S., indicating Brazilians who dispute transactions are often doing so on big-ticket items as well. Brazil has modernized its payments (with PIX and other systems) but credit card fraud and identity theft remain issues, which translate to disputes. Mexico, Colombia, and Argentina also see rising dispute rates, often hindered by patchy address verification and less widespread use of fraud tools among domestic retailers. Additionally, cross-border commerce (U.S. sites selling into LatAm) contributes to disputes due to delivery issues and customer unfamiliarity with foreign charges. PSPs in LatAm markets need to invest in education: many first-time digital consumers may dispute a charge simply because they didn’t recognize the billing statement (a problem solvable with better descriptors or communication). It’s worth noting that card networks have been expanding chargeback infrastructure in LatAm, e.g., introducing online dispute portals in more countries, which, much like in the U.S., could inadvertently drive volumes higher as filing becomes easier.

- Asia-Pacific (APAC): APAC is a study in contrasts. It includes advanced markets like Australia, New Zealand, Singapore, and Hong Kong, as well as developing ones like Indonesia or India, each with different dispute characteristics. Overall, APAC’s chargeback losses are projected around $5.9 billion by 2028, with a rapid 35% growth in volume over the 2025–2028 period, one of the fastest growth rates globally. In mature APAC markets, we see patterns similar to Western countries: Australia, for instance, has an average chargeback value of $91, almost as high as the U.S. Aussies are heavy card users and love online shopping, so disputes naturally follow. New Zealand likely tracks close behind given cultural similarities and shared network infrastructure. Singapore and Hong Kong, as financial hubs, have high card penetration and tech-savvy consumers, they too report increasing friendly fraud cases and more disputes, especially as cross-border e-commerce is extremely common (a Singaporean ordering from a UK site, for example, might charge back if shipping is delayed, thinking it’s fraud). Malaysia and Southeast Asia are interestingm, these markets historically were cash-heavy, but the pandemic accelerated digital payments. Now, PSPs in Malaysia, Indonesia, Thailand, etc., are encountering chargeback issues that more mature markets dealt with years ago. There’s often less consumer awareness in these countries about the chargeback process, which can cut both ways: fewer frivolous disputes (because people don’t know they can perhaps), but also more confusion and mistrust when disputes do occur. As these countries implement stronger consumer protections, we can expect disputes to rise. A case in point: India reportedly saw a 45% jump in chargeback volume in 2024 alone as eCommerce expanded, and banks made dispute filing more accessible. The key for APAC PSPs is to localize strategies, e.g., in Japan, chargebacks are relatively rare due to cultural and regulatory differences, whereas in China, international card chargebacks exist but much of domestic commerce is on platforms like Alipay/WeChat with other dispute mechanisms. However, as Visa, Mastercard, and other networks push deeper into APAC’s emerging markets, they will bring their global chargeback policies with them. The 35% regional surge we’re expecting is a wake-up call to PSPs from Singapore to Sydney: the dispute wave is headed your way if it’s not there already.

- Middle East & Africa (MEA): While not explicitly requested, it’s worth noting MEA is actually projected to see the highest relative growth in chargebacks, nearly 59% increase in volume by 2028 off a smaller base. As card adoption grows in these regions, consumer disputes will follow. Markets like the UAE or South Africa may see more western-level dispute activity soon. PSPs in these regions often operate under stricter fraud controls (many countries have domestic switches and close issuer-merchant ties) but they should prepare for an uptick in first-party fraud as well.

In summary, chargebacks are a global game now. Each region has its nuances, whether it’s U.S. consumers’ propensity to dispute, Europe’s regulatory dampeners, LatAm’s fraud growing pains, or APAC’s digital surge, but everywhere the trend line is up. For a PSP operating globally, this means you can’t apply a one-size-fits-all approach. You might need regional risk teams, tailored merchant education in local languages, and to keep tabs on how local laws (like Europe’s PSD2 or upcoming regulations in APAC) affect dispute rates.

Rethinking Chargebacks: A Strategic Imperative for PSPs

Given the data and trends we’ve explored, it’s clear that PSP leaders must elevate chargeback management from an operational concern to a strategic priority. The old mindset, treat chargebacks as a routine cost, handle them at the risk team level, and move on, will simply not hold up anymore. Instead, PSPs should reframe chargebacks as both a critical risk factor and a potential competitive differentiator. Here’s what that means in practice:

- Proactive Prevention Over Reactive Cleanup: The most successful PSPs going forward will be those who prevent disputes before they happen, rather than simply processing chargebacks after the fact. This requires investment in tools and partnerships that address the root causes of chargebacks. For example, PSPs can integrate real-time chargeback alert systems (like Visa RDR or Mastercard Ethoca alerts) for their merchants, so that as soon as a dispute is initiated, the merchant can be notified and issue a refund immediately, avoiding the formal chargeback. These alerts have proven to stop a dispute from hitting the network, sparing both the merchant and PSP from the hit. It’s a win-win: the cardholder is satisfied (they got their money back quickly) and the merchant avoids a mark on their record. Yet surprisingly, many acquirers have not rolled this out to all but their largest merchants. That needs to change, broad adoption of real-time dispute alerts can drastically cut chargeback volumes. Another preventative measure is improving transaction transparency: PSPs should ensure that merchants use clear billing descriptors and consider tools that share detailed transaction info (like purchase details, merchant logo, etc.) in the customer’s online banking statement. When cardholders recognize a charge (because it says “XYZ Merchants, your monthly fitness box” instead of “PAYMENT*12345”), they are far less likely to call it fraudulent. Issuers are increasingly enabling such transparency features; acquirers should champion their use because it directly reduces needless chargebacks due to confusion.

- Embrace Data and Analytics: PSPs sit on a trove of data across all the merchants they process for. Leading PSPs are now using advanced analytics and AI to identify patterns and predict which transactions are likely to become chargebacks. Machine learning models can flag, for example, if a certain product line or a certain geography is correlating with high dispute rates, enabling the PSP to warn the merchant or take action (like requiring 3-D Secure for those transactions). Some PSPs are even scoring merchant risk in near real-time, so they can adjust fraud rules dynamically if a merchant’s dispute rate starts climbing. This kind of dynamic risk management wasn’t common a few years ago, but with the razor-thin margins in payments, it’s becoming necessary. The payoff is not just fewer chargebacks, but also potentially higher win rates on the disputes that do happen. By analyzing representment data (i.e., the evidence in second-presentments), PSPs can figure out what works to overturn illegitimate chargebacks. For instance, if providing delivery confirmation tends to win “Item not received” disputes, a PSP could automate pulling that evidence for merchants. Some reports suggest AI-driven representment strategies can boost merchant win rates significantly (even up to 70-80% in certain cases), which translates directly into recovered revenue. In short, data is the PSP’s best ally in the fight against chargebacks, both to nip disputes in the bud and to fight them effectively when they occur.

- Rethink Merchant Relationships and Education: In this new era, PSPs should act less like passive transaction processors and more like strategic advisors to merchants when it comes to risk and disputes. That means educating merchants about the tightened network rules (many merchants still don’t realize how much stricter Visa and Mastercard have become). PSPs should be telling their clients: “Keep your dispute ratio below 1% now, not later, here’s how we can help.” Providing dashboards or reports on the merchant’s chargeback rate, reasons for disputes, and benchmarks against peers can spur merchants to take action. It might even be wise to incorporate chargeback performance into the pricing and contract structure: for example, offering lower fees or incentives for merchants that maintain low dispute rates, while reserving the right to charge extra or hold funds for those who consistently exceed thresholds. Some acquirers already do this implicitly; making it explicit can drive behavioral change. Also, there’s a huge need for consumer education which merchants and PSPs can collaborate on: simple things like clearly posting “Contact us for easy returns, don’t charge back!” on receipts or emails can help. Remember, 53% of customers go to the bank first; if we can shave that down by even a few percentage points through better communication and customer service, that’s millions saved. PSPs might facilitate this by building dispute resolution portals or messaging systems that allow cardholders to engage the merchant directly (some fintechs are exploring exactly this, to intercept disputes and resolve them amicably).

- Turn Chargebacks into a Competitive Advantage: This may sound counterintuitive, how can a negative like chargebacks be an advantage?, but consider the PSP that manages to truly excel at minimizing chargebacks for its merchants. That PSP will have lower loss provisions, fewer scheme fines, and happier merchants (since merchants keep more of their sales revenue and pay less in penalties). They can funnel those savings into better pricing or more innovation. Furthermore, in high-risk sectors (travel, digital goods, gaming, etc.), merchants often choose their payment partners based on who will help protect them from fraud and disputes. If you as a PSP build a reputation for proactive chargeback management, that becomes a selling point to win new business. For example, a PSP might advertise: “Our merchants average 0.5% chargebacks, half the industry average, thanks to our advanced fraud AI and dedicated dispute team.” That kind of value proposition will resonate with merchants who are sick of losing revenue to fraud and who fear the compliance blacklist. In essence, tackling chargebacks head-on can differentiate a PSP in a crowded market. On the flip side, ignore the problem and it can become a competitive liability, no merchant wants to be caught off-guard by fines because their PSP didn’t warn them or help them comply.

- Collaboration with Issuers and Networks: Historically, acquirers and issuers have been on opposite sides of the fence in disputes. But the future might demand a more collaborative approach. Networks like Visa and Mastercard themselves are pushing for this, programs like Visa Collaboration (formerly VMPI) allowed merchants (via their acquirer) to send additional info to issuers at the first sign of a dispute, to prevent it from becoming a chargeback. PSPs should leverage these programs aggressively. By working with issuers to share data (purchase details, IP addresses, etc.), some disputes can be stopped because the issuer convinces the cardholder “oh, that charge was legitimate”. In markets like Asia, where domestic networks or bilateral arrangements exist, we might even see PSPs and issuers share fraud blacklists or data in real-time to block fraudulent purchases preemptively, reducing disputes down the line. A cultural shift toward “fighting fraud together” could yield big results. It’s heartening to see that 56% of financial institutions and 59% of merchants reported chargeback volumes rising >10% last year, heartening not because of the rise, but because both sides acknowledge the problem. It’s a shared problem now, and thus requires shared solutions.

Conclusion: Turning the Tide

The economics of chargebacks in 2025 present a formidable challenge to payment processors, but also a catalyst for change. Faced with soaring dispute volumes, tougher network policies, and evolving fraud tactics, PSP leaders must move beyond viewing chargebacks as a back-office headache. Instead, chargebacks should be treated as a strategic KPI, one that signals the health of your merchant portfolio and the effectiveness of your risk controls.

Yes, the picture painted by the data is sobering: global chargebacks climbing at double-digit rates, friendly fraud morphing into an epidemic, compliance thresholds tightening like a vise. But within that challenge lies an opportunity. PSPs that invest in smarter fraud prevention, collaborate across the ecosystem, and champion a culture of low chargebacks will not only save money, they will win loyalty in the market. In a business where margins are thin and trust is paramount, being the processor that actually helps merchants keep what they earn is a powerful differentiator.

It’s also about reframing mindset. A chargeback is not just a loss or a customer hassle; it’s feedback. It’s telling you something, maybe that your merchant’s checkout process is confusing customers, or their product isn’t meeting expectations, or a fraud ring is targeting a weakness in your system. Smart PSPs will listen to these signals and adapt. They’ll push their teams and their merchants to strive for that ideal scenario where disputes are rare, and when they do happen, most are resolved before escalating to formal chargebacks (remember, currently only ~26% get resolved before becoming chargebacks, there’s a lot of room for improvement).

We’re entering an era of “armored” payments where every transaction might need the digital equivalent of a bodyguard (anti-fraud tools, confirmations, etc.), and every dispute is a battle fought with data and diligence. It’s a challenging road, but the cost of inaction is higher. PSP leaders who still think a <1% chargeback rate is an unattainable gold standard need to wake up, soon it will be the bare minimum requirement just to stay in business under Visa/Mastercard’s rules.

Ultimately, rising chargebacks force us to get better, to refine our systems, educate consumers, and innovate in dispute resolution. By confronting the chargeback challenge head-on, PSPs can help shape a more sustainable payments ecosystem. The alternative is to watch the tide rise and react once you’re already underwater. Instead, let’s turn chargebacks from a cost center into a competitive strength. The PSPs that do so will not only protect their bottom line, they’ll earn the trust of merchants and cardholders alike in a way that sets them apart in the marketplace.

In the high-stakes game of payments, chargebacks have become a defining battleground. The time has come for payment processors to reinvent their chargeback playbook, because the economics demand nothing less.