Imagine a fintech customer, Jane, who nearly wires her life savings to a scammer posing as her bank. A fraudster called, warning her of a “fraudulent transfer” and urging her to quickly move funds to a “safe” account, which was in fact the fraudster’s. Across town, a young man in a new online romance is asked to send money for an emergency medical bill; over months, he makes 11 payments totaling £7,500 before realizing the love was a lie. In each case, the instant speed of modern payments allowed money to vanish in seconds. If a bank or crypto platform waits until end-of-day to review suspicious activity, it’s too late, the funds are gone and the victim is left devastated. These scenarios underscore why real-time detection isn’t just a technical upgrade; it’s an urgent necessity to protect consumers from fast moving fraud and scams.

The Rise of Real-Time Fraud Threats

Today’s financial services operate at lightning speed, and so do criminals. With the advent of real-time payment rails (from instant bank transfers to crypto transactions), fraud schemes have evolved to exploit that immediacy. In particular, several scam typologies highlight how fraudsters leverage real-time channels to prey on customers:

- Authorized Push Payment (APP) Fraud: Scams where victims are tricked into sending money to a fraudster’s account under false pretenses. The customer authorizes the payment, believing the lie, whether it’s a fake invoice, a “secure” account transfer, or an investment that doesn’t exist. APP scams have exploded alongside faster payments, in fact, they now account for over half of all fraudulent bank transfer losses in some regions. Because the victim willingly initiates the transfer, the money often becomes unrecoverable almost immediately.

- Money Mule Recruitment: Fraud rings recruit individuals (sometimes unwitting students or job seekers) to serve as “mules” who receive and quickly forward illicit funds, obscuring the money trail. Sophisticated criminals funnel stolen money through a chain of mule accounts within minutes, rapidly moving it beyond the reach of recalls or chargebacks. A victim’s money can hop through several accounts and across borders before they even realize they’ve been conned. Quick identification of mule activity is critical, a delay of even a few hours could mean criminal proceeds disappear overseas, effectively laundered while banks are still processing yesterday’s alerts.

- Romance Scams: Here, fraudsters exploit emotions over an extended period, building trust via dating apps or social media, then leveraging that trust to solicit money under false emergencies. The impact is deeply personal: beyond financial loss, victims often suffer shame and heartbreak. And the financial losses are mounting, one bank’s data showed the average romance scam case lasted ~3 months with 11 separate transfers sent, £7.5k lost on average before the scam was uncovered. These scams often involve multiple transactions that individually may not trigger traditional static rules, but in aggregate form a clear pattern of exploitation. Only by continuously monitoring behavior can institutions catch these patterns early and stop the bleeding.

- Real-Time Scam Coercion: Impersonation and coercion scams happen in real time, for example, a fraudster calls a customer and keeps them on the phone, guiding them through making a large transfer under duress. In one scenario, a retiree received a call from someone claiming to be their bank, urgently warning of a supposed fraud and instructing them to move funds immediately; the panicked victim complied, unknowingly sending money straight to the criminal. This kind of live social engineering is especially dangerous because the fraudster is actively coaching the victim through defeating security steps. Banks have learned to watch for red flags like an active call during an online banking session, which can indicate a scam in progress. If the institution can detect that coercion in the moment, for example, by noticing the customer is on a call and attempting an unusual high-value transfer, they have a brief window to intervene and verify the transaction before irrevocable harm is done.

Each of these scenarios leverages speed and human trust. They illustrate a painful truth: when money can move instantly, the delay between scam and loss is effectively zero. That leaves no room for after-the-fact detection, stopping fraud requires catching it as it happens. This is where real-time anti-money laundering (AML) and fraud monitoring steps in as a crucial shield for consumers.

Batch Detection vs. Real-Time: Missing the Critical Window

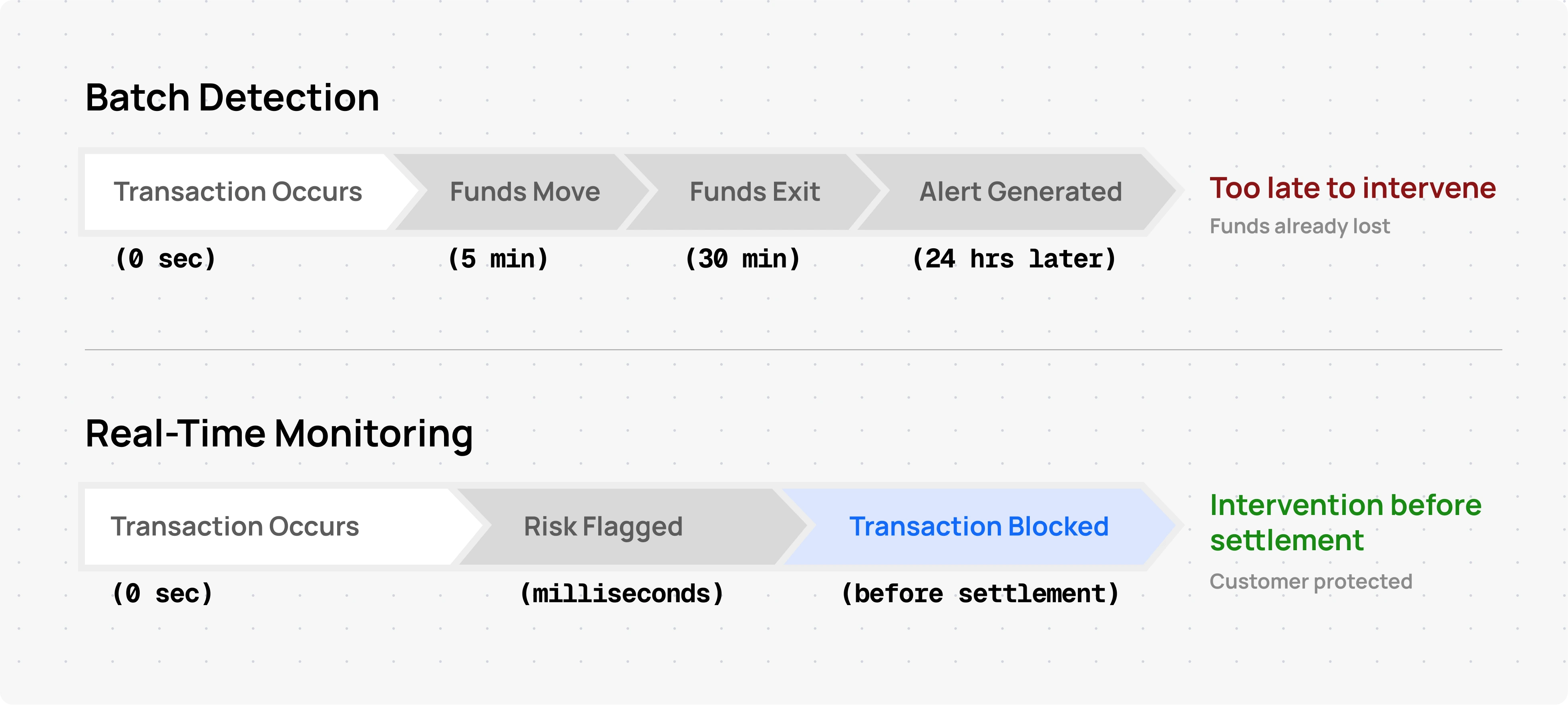

Traditional AML compliance programs often relied on batch-based detection, for example, generating alerts from the day’s transactions overnight, or reviewing suspicious patterns once every 24 hours. In the past, when payments moved slower (or when AML was seen purely as a regulatory checkbox), a delayed review was acceptable. Today it’s a liability. Batch detection means finding fraud after the fact, which is increasingly untenable when facing instant schemes:

- Too Late to Intervene: By the time a batch monitoring system flags an anomalous transfer, hours or days may have passed. For instant payments, those hours are the difference between recovering funds and writing off a loss. In industry terms, “alerts are delayed, potentially hours or days after the transaction, limiting the ability to intervene pre-settlement.” The fraud has long since succeeded, and the customer’s money is gone. In contrast, a real-time monitoring system can flag a high-risk transaction as it is happening and allow the institution to block it before it settles.

- Narrowing the “Replay” Window: Consider how quickly a fraudster can act: a savvy criminal might open a new digital bank account, receive illicit funds, and forward them out through multiple transfers all in an afternoon. Legacy processes that only compile alerts at day’s end will miss that entire sequence. As one Flagright case study noted, “a customer can open an account, transact funds, and close the account all in a single afternoon, much faster than legacy monitoring processes that sorted alerts at day’s end.” In other words, yesterday’s end-of-day checks are woefully outpaced by today’s on-demand banking activity.

- Exploiting the Gaps: Fraudsters are well aware of which institutions rely on static rules or slow reviews. They deliberately design schemes to fall just below thresholds or during off-hours to evade detection. (For example, structuring deposits just under a reporting limit, or initiating scams on weekends when manual review staffing is thin.) If your system only looks at transactions in aggregate after a delay, criminals have a built-in escape route. Real-time systems, on the other hand, offer no such safe lag, every transaction is scrutinized as it occurs, closing the timing gap that criminals have learned to exploit.

In summary, batch detection misses the moment. By the time a compliance analyst sees yesterday’s alerts, victims of APP fraud have authorized payments to scammers, mules have dispersed funds through countless accounts, and the damage is done. This lag not only fails to prevent consumer harm, it can also create a false sense of security, institutions think controls are in place, but those controls are looking in the rear-view mirror. To truly protect customers, detection needs to happen in real time, at the exact moment risk is manifesting.

Proactive Real-Time Intervention: Stopping Fraud in Flight

Real-time monitoring flips the paradigm from reactive to proactive. Instead of investigating suspicious activity after the horse has left the barn, a real-time system raises the alarm during the transaction, when there’s still a chance to stop or divert it. This capability is a game changer for consumer protection. Here’s how real-time AML/fraud detection works and why it makes a tangible difference:

- Continuous, Instantaneous Analysis: A real-time platform evaluates each transaction and event as it streams in, applying rules, behavioral analytics, and machine learning models on the fly. The moment a transaction meets a high-risk criterion (say, an unusually large amount to a first-time payee in a high-risk country), it’s flagged within milliseconds. One compliance handbook sums it up as having “a vigilant security guard at every possible entry point, ensuring each transaction passes stringent checks”. The benefit of this immediacy is clear: potentially malicious or anomalous activity can be identified and acted upon almost instantly.

- Intervening Before Irreversible Harm: Catching an alert in real time enables the institution to take action while the transaction is pending. For example, the bank or platform can automatically hold or delay the payment, trigger an automated step-up authentication, or route the alert to a live fraud analyst within seconds. Many leading fraud teams now orchestrate such responses: if a transfer resembles a known APP scam pattern, the system might “stop execution while raising an alert for investigation, all in seconds.” This quick response is often the only thing standing between a scammer and a victim’s funds. It creates a brief window to contact the customer (out-of-band verification), verify the transaction’s legitimacy, and if needed, stop a fraudulent payment from completing. In effect, the crime is halted mid-flight, not just documented after the fact.

- Real-Time Risk Scoring and Behavioral Signals: Advanced real-time solutions don’t rely solely on static rules; they incorporate a wealth of contextual data to assess each event. This might include device and session behavior (is the user’s device currently on a call while making this transfer? Is there a remote access tool detected on their device?), user history (is this transfer wildly out of character for this customer?), and even consortium intelligence (flags on the destination account from other institutions). By instantly crunching these signals, the system can spot the subtle signs of coercion or fraud that a simple rule might miss. For instance, a sudden surge in online banking session time combined with multiple new payees could indicate a customer being guided by a scammer, a pattern that behavioral analytics can catch in real time, prompting immediate intervention.

- Blocking Rapid Mule Transactions: In a real-time monitoring environment, the moment an account starts acting like a suspected mule, e.g. receiving multiple incoming payments from unrelated parties and attempting quick outbound transfers, alerts will fire. The institution can freeze the account or block the outbound transfers on the spot. As one solution provider notes, “Real-time alerts allow banks to stop transactions before funds exit the network.” This is crucial: it can mean the difference between recovering stolen funds vs. watching them vanish. Stopping a mule in real time not only protects the initial fraud victim’s money, but also prevents downstream victims (and the unwitting mule) from entanglement in criminal activity.

- Empathy and Customer Interaction: Real-time detection also enables a more empathetic response to fraud threats. Instead of merely sending a fraud notification after an account is drained, institutions can reach out to customers in the moment. For example, TSB Bank in the UK credits its real-time scam strategy with saving many customers from romance fraud, by spotting likely fraudulent payments and then personally calling customers to confirm them, they often talk the victim out of proceeding and thus avert disaster. Those compassionate interventions are only possible if the bank’s systems raise an alert immediately when a risky transaction attempt occurs. The result is not just prevented losses, but customers who feel their bank “had their back” in a moment of crisis.

In practice, real-time intervention has proven its worth. We see cases where a fintech’s system flags an unusual $10,000 transfer by an elderly customer to a new crypto exchange account; the transaction is paused and a support rep quickly discovers the customer was on the phone with a scammer, the transfer is canceled and the customer’s funds saved. Or a neobank detects that a brand-new account is performing rapid fire transactions at 2 AM to multiple overseas accounts; within minutes the account is frozen as an apparent mule, protecting downstream victims and the integrity of the platform. None of this would be achievable with after-the-fact controls. Real-time detection turns “moments of truth” into opportunities to safeguard the innocent.

Real-World Impact: How Flagright’s Customers Protect Users

Financial institutions across fintech, crypto, and banking are embracing real-time AML solutions to proactively stop harm to their users. Flagright, a company at the forefront of real-time financial crime compliance, has seen its clients achieve exactly that kind of active protection. Unlike older AML systems that ran only nightly checks, Flagright’s platform enables compliance teams to monitor transactions both in real time and after the fact in one unified system. Suspicious patterns can thus be flagged instantaneously as transactions occur, a crucial advantage for preventing rapid illicit flows. (At the same time, the platform still allows retrospective analysis on historical data, marrying immediate defense with thorough hindsight reviews.)

Flagright’s clients leverage this real-time capability to intervene against fraud and money laundering schemes before they escalate. For example, Dollarize, a fintech serving cross-border transfers, selected a real-time monitoring solution so it can “detect risks before they become threats.” By scoring transactions dynamically and enforcing rules within sub-second response times, the compliance team can instantly spot when something isn’t right, whether it’s a suspicious large transfer out of a customer’s account or a rapid series of deposits that hint an account might be a mule. One Flagright client in digital banking noted that the system’s average API response is ~0.44 seconds, meaning even high-volume transaction streams are screened immediately without slowing down the customer experience. In practice, this has allowed institutions to catch fraud patterns that would have slipped through legacy systems. A customer’s card swipe or wire transfer can trigger an alert and be blocked in real time if it matches a known scam scenario or violates a risk threshold, giving the institution a chance to investigate right away, not the next day.

Equally important, modern real-time platforms like Flagright empower compliance and fraud teams to be agile and creative in protecting customers. With a no-code rules engine and an extensive library of typologies, analysts can quickly deploy new scenarios as soon as they learn of emerging fraud tactics. This agility means when a new scam trend arises, say a spike in “crypto investment” frauds targeting a neobank’s users, the team can implement a rule that very day to flag payments fitting that pattern. There’s no waiting weeks for vendor support or coding a new model. The result is a faster institutional response to protect end-users from the latest threats. As one compliance lead put it, this kind of in-house agility “enables firms to adapt to changing risk scenarios with unparalleled speed,” which directly translates to fewer victims and fewer losses.

The proactive approach adopted by Flagright’s clients is already yielding benefits in customer safety and trust. Instead of apologizing to customers after an attack, these institutions are catching fraud attempts in real time and often preventing any loss from occurring. Every alert handled in real time is a potential life crisis averted, a family’s rent not stolen by scammers, a retiree’s nest egg preserved, a young startup’s funds not siphoned by fraud. And beyond the individual incidents, the data suggests an overarching improvement: firms using real-time monitoring can drastically improve their detection efficiency (catching more true threats) and reduce false positives, freeing up teams to focus on genuine danger. In short, real-time AML isn’t just stopping crime, it’s enabling a higher standard of customer service and security.

From Compliance to Protection: AML’s Evolving Mission

Perhaps the most profound shift in the modern approach to AML and fraud prevention is a change in mission. Traditionally, AML programs were seen as compliance-driven, the goal was to satisfy regulators by filing reports and avoiding fines. Stopping fraud was important, yes, but often viewed as a cost of doing business or outside the strict mandate of compliance. That era is over. Today, regulators and industry leaders increasingly recognize that preventing consumer harm is just as important as ticking the compliance boxes. Modern AML is not just about paperwork, it’s about protecting people.

This shift is evident in emerging regulations and expectations. In some jurisdictions, authorities are explicitly pushing banks to take on more responsibility for safeguarding customers from scams. For instance, the UK is now mandating reimbursement for many APP fraud victims, effectively pressuring banks to prevent those scams in the first place (since they may end up paying for the losses). Regulators are asking, in essence, “Could the bank have seen this fraud coming and stopped it?” and if the answer is yes, inaction is no longer acceptable. As one analysis of Europe’s fraud trends put it, “billions disappearing via authorized scams with little recourse for victims is not a sustainable state of affairs…there is mounting pressure to prevent such fraud or stop it mid-flight.” Financial institutions that once might have shrugged off scams as “customer-authorized, not our fault” are now being challenged to intervene and protect the customer as a duty of care.

Global frameworks too are blending fraud prevention into AML obligations. The newly adopted EU Instant Payments Regulation requires that by 2025, most payments providers implement measures like account name matching (Confirmation of Payee) before executing an instant transfer, a safeguard squarely aimed at thwarting impersonation scams in real time. It also pushes for real-time screening of transactions against AML criteria during instant payments. In other words, real-time fraud controls (traditionally the domain of “fraud teams”) are being written into compliance requirements, and vice versa. We’re seeing a convergence of AML and fraud disciplines around the shared goal of protecting the financial system and its users in real time. As a report on money mules noted, “new regulations are placing significant importance on real-time monitoring...challenging anti-fraud departments to detect mule networks before any harm is caused.”

Crucially, the business mindset is changing in tandem. Forward-looking fintechs and banks now treat customer protection as mission critical, not as a cost center. Every prevented scam not only saves the customer from trauma, but also saves the institution the costs of reimbursement, investigation, and reputational damage. It’s far cheaper (and better for brand loyalty) to block a fraudulent payment than to explain to a customer why you didn’t. And when something does slip through, institutions are increasingly expected to make the customer whole, adding financial incentive to get prevention right. As one industry commentary observed, the surge in scams “underscores the urgent need to elevate fraud detection and intervention from a cost center to a core component of user protection. The focus must now pivot to advanced, real-time analytics to stem the flow of money before it leaves the victim’s account, not just after the fact.”

Modern AML, therefore, is inherently about active consumer protection. Compliance and fraud teams are becoming guardians of customers, leveraging real-time tools to watch over transactions and step in at the first sign of danger. This is a mission that blends technology, empathy, and duty: technology to analyze and act in milliseconds, empathy to understand the human stories and reach out to victims, and a sense of duty to do the right thing by customers and the wider community. A bank or fintech that stops a scam in real time isn’t just avoiding a loss, it’s potentially saving someone from ruin, preserving a family’s trust in the financial system, and undermining criminal enterprises at the roots.

In conclusion, real time detection is critical for consumer protection because it aligns the entire financial crime effort with its most important outcome: keeping people safe. It enables institutions to be there in the moment that counts, rather than arriving after the damage. For compliance, fraud, and risk teams at fintechs, crypto platforms, neobanks, and banks, adopting real-time monitoring is more than a tech upgrade, it’s a commitment to a more proactive, compassionate form of finance. It’s about saying we won’t wait while our customers are in harm’s way. With real-time AML in place, modern financial institutions can intervene when it matters, stop fraudsters in their tracks, and uphold the promise that underpins all banking: your money is safe with us. In an era of faster payments and faster fraud, that promise can only be kept through vigilance that is as real-time as the threats we aim to prevent.