.webp)

Financial institutions are facing a surge in fraud and financial crime, but real-time transaction monitoring is emerging as a powerful solution with tangible ROI. Regulators are increasingly urging banks and fintechs to monitor transactions before they’re executed rather than after, aiming to stop illicit activity in its tracks. This shift comes as money keeps moving faster; real-time payments and instant transfers are now common, and criminals have been quick to exploit these faster channels. In 2024, U.S. consumers reported over $12.5 billion in fraud losses, a 25% jump from the prior year, and globally losses from scams top $1 trillion with only ~4% ever recovered. Clearly, the stakes for fraud prevention are enormous. Real-time transaction monitoring not only helps meet these new challenges, it delivers compelling return on investment by dramatically reducing manual workloads, accelerating throughput, and improving legitimate approval rates. Below, we break down the ROI case for real-time monitoring, backed by customer data and industry trends.

The Case for Real-Time Monitoring: From Regulators to Risk Reduction

Regulators are moving the needle toward real-time AML monitoring, recognizing that the old after-the-fact approach is no longer enough. In 2021 the European Banking Authority (EBA) issued guidelines urging a risk-based approach to pre-transaction monitoring, meaning firms should decide which high-risk transactions to monitor in real time and intercept if needed. The logic is simple: while traditional AML systems flag suspicious activity only after a transaction is completed, real-time systems can detect and block suspicious payments before the money moves. This paradigm shift is gaining traction: Bank of Valletta in Malta became one of the first banks in the EU to adopt real-time AML monitoring with AI, aiming to prevent money laundering before execution. Regulators and banks alike see that “following the money at the same speed as it moves” is key to fighting modern financial crime.

However, implementing real-time monitoring isn’t trivial. Deciding if a transaction is suspicious within a fraction of a second requires rich data and intelligent automation. Solutions must instantly scan transactions against rules, customer profiles, and external data. To meet the challenge, advanced platforms like Flagright’s are engineered for high-performance, sub-second risk scoring. In practice, this means scanning a transaction across large datasets and machine learning models in perhaps 300-500 milliseconds. Flagright’s API-driven monitoring engine, for example, can score transactions in mere milliseconds and return a decision (approve, block, or flag) almost instantly. This level of performance is now a real differentiator, it aligns with regulatory expectations for proactivity while ensuring customers don’t experience undue delay.

Cutting Manual Reviews and False Positives - A Direct Cost Savings

One of the most immediate ROI drivers for real-time monitoring is the sharp reduction in manual compliance workload. Traditional transaction monitoring systems are notoriously inefficient, flooding compliance teams with false-positive alerts. Industry research finds that over 95% of AML alerts are false positives, consuming about 42% of compliance resources on needless reviews. Rules-based monitoring engines often generate 90%+ false positives, creating alert fatigue and mountains of work for analysts. In fact, between 2016 and 2023, the hours spent on compliance jumped 61%, and some institutions quadrupled their compliance headcount to keep up. This manual-heavy approach drives up costs and is ultimately unsustainable.

Real-time, intelligent monitoring flips this script by drastically reducing alert volumes and automating low-level review tasks. Flagright’s platform, for instance, combines a powerful rules engine with AI “forensics” agents to filter out noise. The results have been striking, some Flagright clients saw an 87% reduction in manual monitoring efforts after implementation. Sciopay, a fintech lender, provides a concrete example: by deploying real-time transaction monitoring, they achieved an 87% drop in manual alert reviews, saving each compliance analyst about 115 minutes per day that would have been spent on tedious investigations. In other words, what used to consume two hours of an analyst’s daily shift is now handled automatically. This translates to major labor cost savings and allows a leaner team to manage even growing transaction volumes.

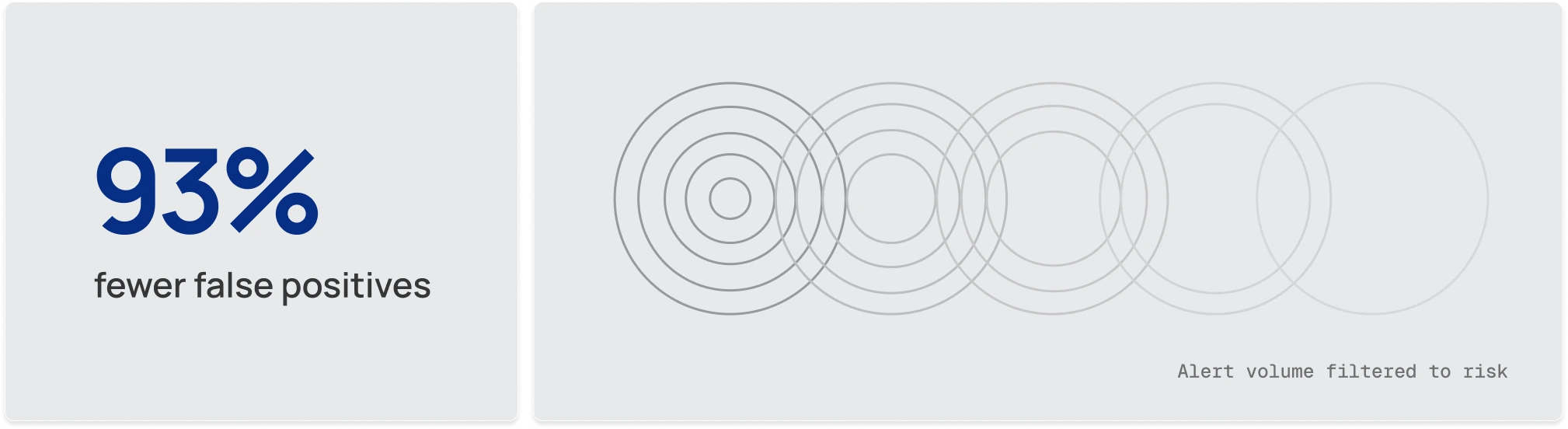

Moreover, better precision means fewer alerts in the first place. Flagright reports that organizations using its real-time screening and monitoring have cut false positive alerts by up to 93%. By using smarter detection models and risk-based rules, the system flags only truly suspicious behavior with greater accuracy. Fewer false alerts = fewer cases to review = lower operational costs. Instead of dozens of analysts sifting through thousands of “ghost” alerts, a smaller team can focus on the handful of truly risky cases. This not only saves money on personnel but also improves compliance effectiveness (real threats are less likely to be missed in the noise). An added benefit is improved analyst morale and retention, highly skilled staff are no longer buried in routine tasks like rubber-stamping false hits, but can focus on meaningful investigations. All these efficiency gains contribute directly to ROI, often allowing financial institutions to “right-size” their teams and avoid continuously expanding headcount just to keep up with alerts.

Sub-Second Decisions: Speeding Up Throughput Without Sacrificing Security

Another angle to ROI is the throughput and customer experience benefits of real-time decisioning. A common concern is that compliance checks might slow down business, e.g. transactions held for review or delayed until next-day batch processing. Real-time transaction monitoring addresses this by operating instantaneously in the flow of transactions. With a modern API-based system, risk checks occur in realtime as part of the transaction authorization process, typically in well under a second. Flagright’s high-performance architecture, for example, boasts sub-150ms response times for scoring a transaction , that means a fraud or AML risk decision comes back faster than a blink of an eye.

For legitimate customers, this speed translates to a frictionless experience. A low-risk payment isn’t needlessly held up waiting for compliance approval, the monitoring engine clears it nearly instantly. As Flagright notes, its real-time engine can “assess transactions as they happen and enforce decisions instantly via API”, letting good customers proceed without any noticeable delay. The result is higher throughput: your business can safely process more transactions in the same amount of time, because there’s no bottleneck of manual checks. For instance, instead of generating a batch of alerts overnight (and potentially pausing those accounts or funds until review), a real-time system evaluates each transaction on the fly. Suspicious activity is halted immediately, preventing losses while everything else sails through. This minimizes the opportunity cost of fraud controls by accelerating legitimate activities rather than slowing them down.

From an ROI perspective, faster throughput and less friction can directly impact revenue and growth. Higher approval rates mean more transactions (and fees) completed instead of declined. In sectors like payments or e-commerce, every false decline or delayed transaction risks losing a customer or sale. By reducing false positives ~93% and only stepping in when truly necessary, real-time monitoring ensures fewer “false declines” that frustrate customers. For example, a traditional system might flag a perfectly valid customer payment for review (“payment delayed for compliance checks”), with real-time intelligent scoring, such cases are far less frequent, so more good transactions go straight through. This boosts customer trust and retention, which is hard ROI to quantify but very real. In fact, over-alerting and unnecessary intervention carry a hidden reputational cost; if customers often get stuck in compliance checks or have legitimate payments blocked, it erodes their confidence. Real-time monitoring avoids that scenario, helping preserve your institution’s reputation and customer loyalty while still catching the bad actors.

Additionally, the ability to intercept fraud in real time prevents direct losses and fraud costs. Once a fraudulent transaction is executed (especially in instant payment networks), recovering funds is difficult. Stopping a fraudulent payment before it completes therefore saves money that would have been written off as a loss. It also spares the business from downstream costs like chargebacks, reimbursement of victims, or regulatory penalties for allowing illicit transactions. In a 2025 survey, 79% of organizations reported being hit by payments fraud attempts in 2024, so nearly every company is a target. Those with robust real-time defenses can thwart many of these attempts, directly cutting down fraud losses that would otherwise eat into profits.

Finally, speed and automation give scalability benefits. As your transaction volume grows, a real-time automated monitoring system can handle the load without a linear increase in compliance staff. This scalability was historically a pain point, many fast-growing fintechs found their manual compliance processes couldn’t keep up, forcing them into costly hiring sprees or tech overhauls. With an API-first, automated solution, one Flagright client managed to integrate and go live in just 2 weeks, and thereafter they could support their growth without massive new hiring. Such agility and scalability mean future cost avoidance, you’re less likely to face a crisis of having to suddenly triple your compliance team or pay for a new system when volumes spike or regulators tighten standards.

Higher Approval Rates and Better Customer Outcomes

Real-time transaction monitoring also drives ROI by improving approval rates and overall business performance. This ties closely to the reduction of false positives mentioned earlier. In legacy setups, compliance rules often cast a wide net to avoid missing anything risky, which inadvertently snags a lot of legitimate activity (false alarms). The fallout is that many perfectly good transactions get flagged for review or declined “just in case.” Every one of those unnecessary interdictions is potentially lost revenue, the customer might abandon the transaction or the extra friction might push them to a competitor over time. It’s also a brand issue: if your service gains a reputation for blocking customers or making them jump through hoops, you’ll lose goodwill.

By contrast, real-time monitoring systems using advanced analytics are far more precise. Flagright’s platform, for example, dynamically scores transactions and customers based on a myriad of risk factors in real time. Because it has a richer, up-to-the-moment picture, it can often allow transactions that an older static rule system might have flagged. The result is higher legitimate approval rates, more genuine transactions get approved on the first pass without manual intervention. In practical terms, if your previous approval rate for, say, online payments was 95% (with 5% flagged/held), you might improve that to 98-99% approved with a smarter real-time system, with only the 1-2% truly suspicious ones being stopped. Those extra successful transactions directly contribute to revenue or throughput. And as mentioned, customers enjoy a smoother experience, which builds trust and can increase their lifetime value (happy customers are more likely to use your service more and refer others).

It’s worth noting that higher approval rates don’t come at the expense of risk, quite the opposite. By catching the right signals in real time, institutions can be more aggressive in approving good customers while still blocking bad actors swiftly. For example, real-time monitoring can instantly cross-check a payment against sanctions lists, behavioral anomalies, and device or identity data. If nothing looks risky, it passes it immediately (where a blunt rule might have flagged it due to one minor threshold). But if something is truly suspicious (say it triggers a combination of high-risk factors), the system can block or hold it milliseconds after the customer clicks “send”. This kind of intelligent, risk-based decisioning ensures you stop fraud and laundering attempts before funds leave your institution, potentially saving huge downstream costs. It also keeps regulators satisfied, you can demonstrate that even as you approve more good transactions, you’re actually improving risk control by focusing on the real threats. In the long run, that means fewer regulatory issues or fines (which are themselves a massive cost; major AML fines and enforcement actions can cost tens of millions and cause reputational harm).